by Gary Alexander

August 1, 2023

In 1849, the Scotsman Thomas Carlyle dubbed a new study called Economics, “The Dismal Science,” partly because a famous economist (really a doomsday preacher) Thomas Malthus said we would all starve to death, and a few Scrooges tried to justify sweatshops and slavery under the false flag of profits.

That calumny continued in the 20th Century in the major definitions of economics, which focused on scarcity. Paul Samuelson, author of the dominant economics textbook since 1948, defined economics as “the study of how societies use scarce resources to produce valuable commodities and distribute them among different people.” British economist Lionel Robbins echoed that line: “Economics is the science which studies human behavior as a relationship between ends and scarce means with alternative uses.”

Our favorite economist, Ed Yardeni, begs to differ. In his 2018 book Predicting the Markets, he writes:

“I’ve learned that economics isn’t a zero-sum game, as implied by the definition [cited above]. Economics is about using technology to increase everyone’s standard of living. Technological innovations are driven by the profits that can be earned by solving the problems posed by scarce resources. Free markets provide profit incentives to motivate innovators to solve this problem.

“As they do so, consumer prices tend to fall, driven by their innovations. The market distributes the resulting benefits to all consumers. From my perspective, economics is about creating and spreading abundance, not about distributing scarcity.” – Ed Yardeni, in “Predicting the Markets”

I have long argued the same point, and now we hear a similar retort to the mantra of “scarce resources” in a July 21 Op-Ed in the Wall Street Journal, “We Will Never Run Out of Resources,” by Marian L. Tupy, co-author of “Superabundance: The Story of Population Growth, Innovation and Human Flourishing on an Infinitely Bountiful Planet” and David Deutsch, author of “The Beginning of Infinity: Explanations that Transform the World.” Recall Thomas Malthus, that dismal economist who wrote in 1798 that people reproduce geometrically (2-4-8-16), while food only grows arithmetically (1-2-3-4), netting famine. Tupy and Deutsch point out that the global population has grown 8-fold since he wrote that (geometrically, that is 2 to the 3rd power) while food has grown far more than 10-fold, netting a super-abundance of food.

By the way, I have one word to defy Malthus: Chicken! Is chicken food or population? Answer me, Tom!

Furthermore, the authors argue that the world hasn’t run out of a single metal or mineral, while “proven resources” of most have grown due to technological improvements in finding those resources, motivated by higher prices – the reward for finding those resources. “Geologists have surveyed only a fraction of the Earth’s crust, let alone the ocean floor. As surveying and extracting technologies improve, geologists and engineers will go deeper, faster, cheaper and cleaner to reach hitherto untouched minerals.”

Eventually, materials will run out, of course, and that’s why we’re using less of almost everything. Our technological revolution calls for miniaturization – smaller and lighter everything. We’re using less wiring in our wireless society and much lighter packaging, with less need for travel, too. Knowledge is the ultimate resource and that comes from human ingenuity more than mining deeper into earth’s crust.

Sadly, Most Economists are Still Dismal (and Therefore Mostly Wrong)

In my 55+ years of following major economic gurus, I was seduced by the voices of doom for a quarter century until I realized they were mostly wrong. It’s seductive (and strangely “hip” or “cool”) to be more negative and cataclysmic in your predictions than the next guy. It’s strategically smart to corner the low end of the market prediction sweepstakes. The Dow will fall 30%…no, it will fall 50%, Oh, why not 90%!

Well, I wised up in 1990 and formed the whimsical organization “Apocaholics Anonymous” for former prophets of doom who wised up. So far, nobody else has joined my organization of reformed doomsday writers. True to form, in the past year nearly every pundit predicted a recession, and no such recession has happened….yet. Most notably, the prestigious Conference Board reported on April 12, 2023, that the probability of a recession was “near 99 percent … within the next 12 months,” reasoning that, “the Federal Reserve’s interest rate hikes and tightening monetary policy will lead to a recession in 2023.”

As I reported recently, economists are finally backing off of that consensus (see the July 15, 2023 Wall Street Journal, “Economists Are Cutting Back Their Recession Expectations”), but that recent Journal survey still finds that 54% of economists still expect to see a recession in the next 12 months, down from 61% in the prior two surveys (the latest survey was conducted July 7-12, just before the June 3% CPI was released on July 12, showing only a 3% year-over-year inflation rate increase, vs. 9.1% in June of 2022).

The most concentrated agglomeration of dismal economists may be at the Federal Reserve Board in Washington, DC, which is staffed by 400 or more dismal PhD economists, and they have also long been forecasting a recession – at every FOMC meeting this year. As Ed Yardeni summarizes their reports:

“The January FOMC minutes noted: ‘The sluggish growth in real private domestic spending expected this year and the persistently tight financial conditions were seen as tilting the risks to the downside around the baseline projection for real economic activity, and the staff still viewed the possibility of a recession sometime this year as a plausible alternative to the baseline.’ The March FOMC minutes indicated that a mild recession forecast was now the staff’s baseline: ‘Given their assessment of the potential economic effects of the recent banking-sector developments, the staff’s projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.’ That outlook held firm in the May FOMC minutes and June FOMC minutes.”

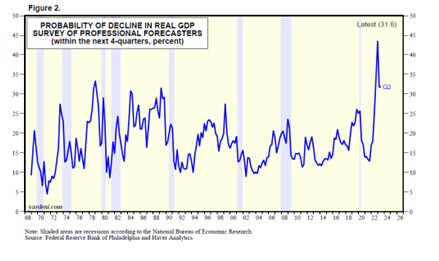

Another sign of dismal prospects is the Philly Fed’s Survey of Professional Forecasters, also known as the “Anxiety Index.” This survey asks a panel of experts to estimate the probability that real GDP will fall in the current quarter and each of the following four quarters. That’s a pretty high bar of pessimism – four declining quarters in a row. The average probability over the last 50 years runs at about 20%. Well, the Q2 estimate was 31.8%, down from the previous all-time high over 40%, worse than even 2008 or 1979.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Economists may be chronically dismal, but a true understanding of economics begets prosperity.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

Four Key Sectors to Consider Now

Income Mail by Bryan Perry

The Fed’s Latest Rate Increase and Its Impact on Regional Banks

Growth Mail by Gary Alexander

Economics – The Bountiful Science

Global Mail by Ivan Martchev

The Last ZIRP Man Standing

Sector Spotlight by Jason Bodner

To Broadcast the Truth the Loudest… Whisper It

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20 years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.