by Louis Navellier

July 7, 2026

On our 250th national birthday – when thousands of soccer fans from Europe, Africa, Latin America and elsewhere are seeing the “real America” in a new and positive light – the European press is dominated by stay-at-home skeptics, especially some poison pens writing for the British and other European media.

I realize Europe has been sizzling hot and miserable lately, but that is no reason to keep trashing America.

Let me give you an example of the negative media emanating from Britain: The Telegraph reported: “The Bank for International Settlements (BIS) said on Sunday that ‘excessive’ spending on new AI data centers and opaque transactions risked a financial meltdown similar to the global credit crunch nearly two decades ago. The BIS, known as the bank for central banks, said there was growing ‘peril’ in financial markets from the complex web of financial ties between AI giants, shadow banks and data center builders unravelling.” The BIS also said, “Financial stability could … be at risk in the event of an AI bust.”

European Central Bank (ECB) President Christine Lagarde said the same thing in a speech in Vienna, implying AI will trigger a financial crisis! But our new Fed Chair, Kevin Warsh, attended an ECB Forum in Portugal last week, and I suspect he chatted with Lagarde privately about her misinformed scare tactics, since Warsh argues, within the Fed and amid central bankers, to the effect AI is boosting productivity and U.S. non-inflationary GDP growth, so central bankers should not worry so much about our strong GDP growth rates and a rising dollar.

At the ECB Forum last week, after repeated questions from moderator Sara Eisen, Chairman Warsh refused to provide forward guidance on rates, since he had previously declared that such guesswork about the future is not allowed under his new Fed regime. A more significant thing Warsh said was the Fed would let financial markets dictate Fed policy. Essentially, that means if Treasury yields decline, the Fed would follow and cut key interest rates. This was not an outrageous statement by Warsh, but more of an acknowledgement that the bond vigilantes (the large institutional investors) will continue to influence Treasury yields and any future central bank policy.

In the meantime, a technology war between Europe and the U.S. persists. President Trump recently said:

“Numerous European Countries have been discussing the imminent implementation of a Digital Services Tax on American Companies. Some of these countries are close to actually doing this. Please let this presidential statement serve to represent that any Country that imposes such a Tax will immediately be met with a 100% TARIFF on any and all Goods sent to the United States of America. This TARIFF will supersede Trade Deals made with the Country, whether implemented, signed, or not. Additionally, the 100% TARIFF will be immediately imposed, if they proceed.”

Apparently, we are at war with the EU, as the fight over taxing American technology companies persists!

So, we have a choice, America. We can oppose air conditioning and data centers, like they do throughout much of Europe, or we can instead be comfortable (via air conditioning) and prosper (from AI and data-center investments). We can choose to complain about everything and blame technology companies, or we can follow the leaders and get rich along with them. In the end, we have to decide whether we want to complain or grow and prosper. I have chosen to grow and prosper. The current economic and market environment is the best since 1999 and it would be a shame if investors listened to the army of naysayers and missed out on the best stock market environment in almost 30-years. I hope you share my outlook.

In other global news, the Iranian Revolutionary Guards Corp (IRGC) attacked two ships traveling through the Strait of Hormuz and the U.S. Navy responded with overwhelming force, so, at this moment, the cease-fire between Iran and the U.S. is back on, and WTI crude oil prices have fallen to around $70 per barrel.

Several countries are striving to replenish their depleted crude oil inventories, so worldwide demand is expected to remain strong for the next few months. Europe’s LNG inventories are at a 15-year low and have likely been exasperated by the recent heat-wave, so that bodes well for U.S. LNG exports. Although the Middle East situation is not yet normal, commerce is picking up and energy volatility has diminished.

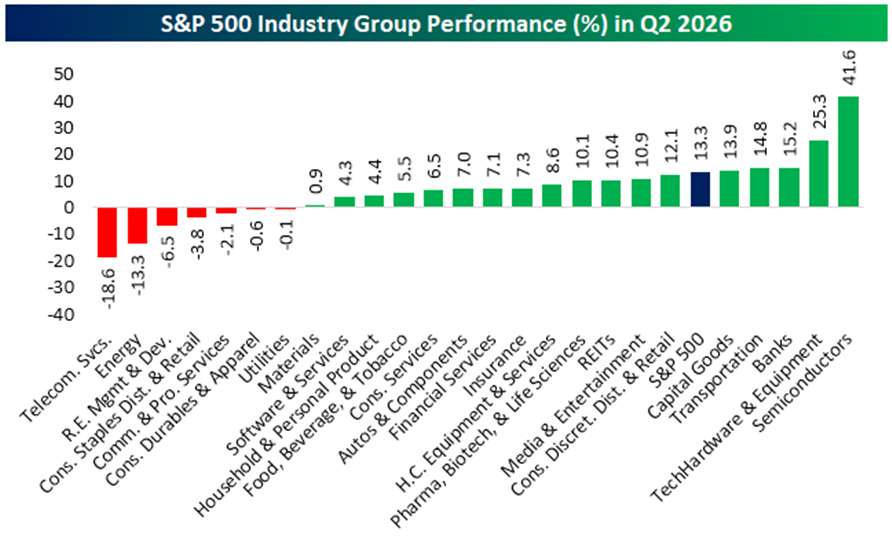

Second Quarter Sector Analysis – Led by Semiconductors

Although energy-related inflation is receding, a new problem is AI-related inflation after Apple raised the price of its computers and iPads due to the higher cost of memory. Apple has not yet raised the price of its iPhones, but price increases are anticipated for its new iPhones in September. Microsoft reduced the RAM in its surface laptops to avoid a price increase, but if you add the RAM back in, the price increases.

While some investors are worried about price increases, we are profiting from higher memory prices. Micron Technology’s revenues surged 346% to $41.46-billion vs. $9.3-billion in the same quarter a year ago. During the same period, the company’s earnings soared 1,368.5% to $28.24-billion or $24.67 per share compared to $1.89-billion or $1.68 per share! Micron also raised its quarterly guidance to around $50-billion in revenue, well above consensus estimate of $43.2-billion, so the tech boom is for real.

Please don’t worry about the recent sell-off in AI and data-center-related stocks late last week. The Financial Times reminded us, “In the U.S., AI plays constitute more than 40% of the market cap and have constituted 80% of returns this year. The return and concentration is similar in Japan and even more extreme in South Korea and Taiwan.” Those who unload their AI and data-center stocks literally have no better place to go, since spectacular returns are forecasted. For example, Micron Technology now trades at just 7.4 times forecasted 2027 earnings, while Nvidia trades at 15.3 times forecasted 2027 earnings. As a result, any dip in the AI and data center related stocks is a screaming buy!

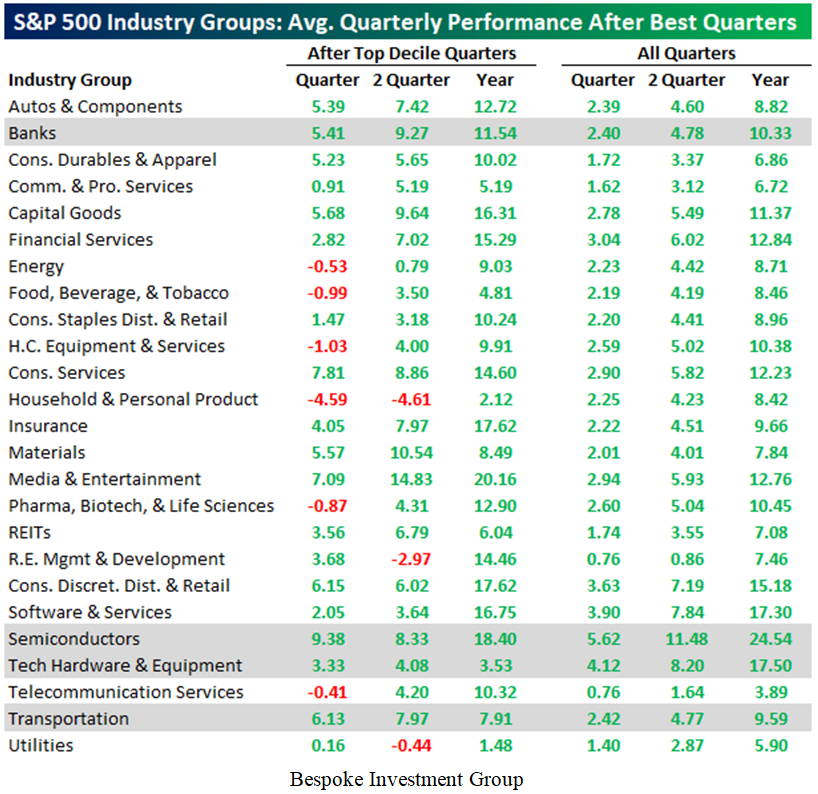

When I say investors have “no better place to go,” I mean it. Our friends at Bespoke documented the S&P 500 returns in the second quarter were driven by Semiconductors (up 41.6%), followed by Technology Hardware & Equipment (up 25.3%). Historically, when these two-sectors have performed strongly:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

CNBC continues to throw cold water on the AI boom. For example, they interviewed aging permabear Jeremy Grantham, who said, “This is the most expensive market in American history.” On CNBC’s Squawk Box, Grantham said, “Based on the value of the stock market compared to GDP, with modifications, this is the most expensive market in American history.”

Folks, this is nonsense. First, Jeremy Grantham is a bond investor who has never liked stocks, to my knowledge. Secondly, Grantham does not look at earnings growth, order backlogs, analyst earnings revisions, earnings surprises and forecasted price-to-earnings ratios – so why would CNBC have such an un-American, negative naysayer on Squawk Box? Thankfully CNBC’s Joe Kernan gave Grantham a good grilling, pointing out he has been bearish since 2010 and wrong ever since then with his stock forecasts.

The U.S. Job Situation – Updated

On Wednesday, ADP reported 88,000 new private payroll jobs created in June, well below the economists’ consensus estimate of 110,000. Small, mid-size and large businesses all added jobs in June, according to ADP. According to Challenger, Gray & Christmas, a global outplacement firm, employers based in the U.S. announced about 45,000 job cuts in June, down 53% from the 97,000 layoffs in May, so the job market is steadily improving, which is good for improving consumer confidence and GDP growth.

Since Friday was a government and market holiday, the Labor Department issued their monthly jobs report on Thursday, saying there were 57,000 payroll jobs created last month, far below the economists’ consensus estimate of 115,000. April and May payrolls were revised down by a cumulative 74,000. The jobless rate was 4.2% in June, down from 4.3% in May, due to 720,000 people leaving the labor force.

There was a large drop of 61,000 jobs in leisure and hospitality – the largest monthly decline since 2020. This was largely responsible for the lower-than-expected June payroll totals. The Labor Department said this drop in leisure and hospitality workers reflected “weaker than usual seasonal hiring.”

The good news is manufacturing and construction employment increased, indicative of the AI data center building boom – accounting for more than 50% of construction in the U.S. last month. In June, average hourly earnings rose by 13 cents (+0.35%) to $37.64 per hour and are up 3.5% in the past year.

Treasury yields declined slightly in the wake of this weaker-than-expected June payroll report.

In other economic news, the Institute of Supply Management (ISM) announced its manufacturing index slipped to 53.3 in June, down from 54 in May, but any reading above 50 signals an expansion and this is the sixth month in a row that the ISM manufacturing index has been expanding. The new orders component remained strong at 56 in June, down from 56.8 in May. Interestingly, the price component plunged to 73 in June, down from 82.1 in May. This was the largest monthly drop in the price component in almost four years (since July 2022) and is signaling that commodity inflation is cooling off! Fully 14 of the 17 manufacturing industries that ISM surveyed reported an expansion, which is a good sign.

Navellier & Associates; own Nvidia (NVDA), Micron Technology, Inc. (MU), Apple Inc. (AAPL), Microsoft Corporation (MSFT) and Alphabet Inc. Class A & C (GOOGL) in managed accounts. Navellier and his family own Nvidia (NVDA), Micron Technology, Inc. (MU), Apple Inc. (AAPL) and Alphabet Inc. Class A & C (GOOGL) via a Navellier managed account and Nvidia (NVDA) and Apple Inc. (AAPL) in a personal account. They do not own Microsoft Corporation (MSFT) personally.

All content above represents the opinion of Louis Navellier of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

Europe Keeps Attacking America, Despite our Big Birthday Party

Income Mail by Bryan Perry

Emerging Market Debt Now Seen As a “Go To” for Income

Growth Mail by Gary Alexander

America is Still the Economic Engine of the World

Global Mail by Ivan Martchev

This Tech Rotation is as Bad as it Gets

Sector Spotlight by Jason Bodner

Ignore the Headlines – Focus on the Inner Market Data

View Full Archive

Read Past Issues Here

Louis Navellier

CHIEF INVESTMENT OFFICER

Louis Navellier is Founder, Chairman of the Board, Chief Investment Officer and Chief Compliance Officer of Navellier & Associates, Inc., located in Reno, Nevada. With decades of experience translating what had been purely academic techniques into real market applications, he believes that disciplined, quantitative analysis can select stocks that will significantly outperform the overall market. All content in this “A Look Ahead” section of Market Mail represents the opinion of Louis Navellier of Navellier & Associates, Inc.

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.