by Gary Alexander

July 25, 2023

With all eyes focused on the Fed’s interest rate decisions and M2 mopping-up operations (cutting M2 money supply by about $1 trillion), most pundits ignore our bloated Baby Boomer population bomb now in transition from The Great Society into their Golden Years on the long Glide Path to the Great Beyond.

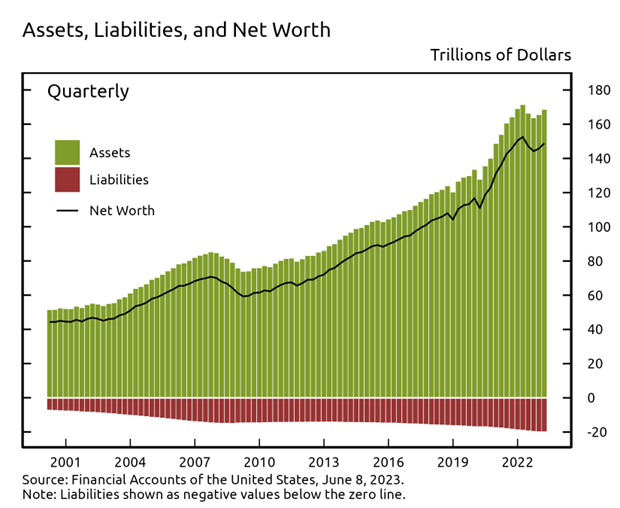

We keep hearing about those “mountains of debt” growing higher, but how often do we hear about the 90% of that iceberg that lies beneath the surface, the unseen wealth supporting that debt. “Net worth” is what those two words imply – the net value of one’s estate after accounting for all debts. That figure is now over $150 trillion (about $450,000 per person), according to the Fed’s accounting. In this chart, the debt line on the bottom is growing, but the green giant is growing faster, and few pundits talk about it.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

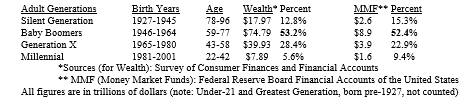

If you want to focus on a single generation that won the asset lottery, it’s the campus protestors that began invading the planet the year after I was born (1945), called the Baby Boomers. I’m the last of the “Silent Generation,” although I refuse to be silent about the silliness of that name for my generational cohort.

Here’s the breakdown of the birth ranges and the generational wealth and cash we all now control:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Note that Baby Boomers control over half the nation’s wealth, including over half of all cash in Money Market Funds. Not bad for those who once lectured about the evils of capitalism. Time to shop, Boomers!

Born 1946 to 1964, Baby Boomers are now 59 to 77. How did they pull this caper off? I’d call it good luck in a three-part trifecta of good timing involving a stock boom, wage inflation, and a peace dividend:

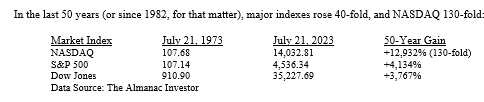

#1: Stock market savings. Baby Boomers entered the work force about the time stocks took off, so they rode the greatest bull market of the century. Near the stock market’s nadir in the mid-1970s, three seeds of future gains were sown: (1) the birth of super-charged NASDAQ stocks in 1971; (2) ERISA in 1974 gave birth to self-directed 401(k) pension plans; and (3) discount brokers were born May 1, 1975, allowing low commissions and self-directed accounts, allowing us all to control our own investing fate.

In the last 50 years (or since 1982, for that matter), major indexes rose 40-fold, and NASDAQ 130-fold:

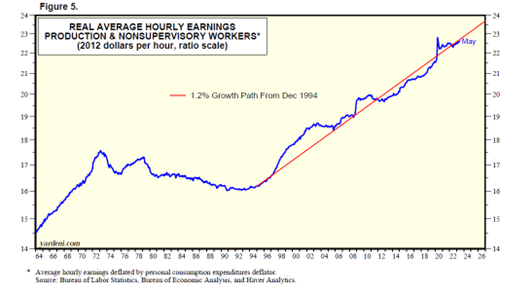

#2: Wages rose, first through inflation, then through business expansion. In their youth, many Baby Boomers were campus radicals who didn’t trust anyone over 30, storming the Bastille of the capitalist system. Sure enough, they suffered through their parents’ Keynesian follies run amok in the 1960s and the stagflationary 1970s, but then we all started climbing the wage ladder, as real wages soared in the ‘90s:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

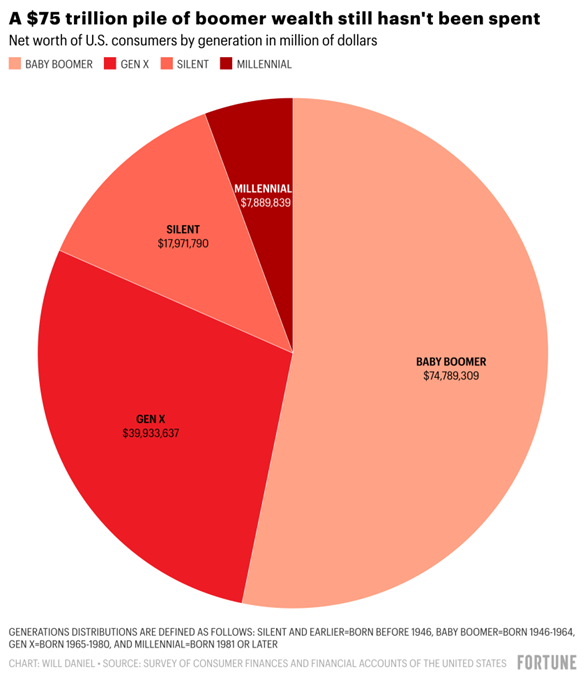

#3: Good Geopolitical Timing: The Green Revolution, the end of the Cold War, and the Tech Boom delivered a Peace Dividend, so the Baby Boomers became Stock Market Lottery Winners, garnering something like $75 trillion in assets to play around with in their final years, and $9 trillion in ready cash assets to throw into the stock market, or Las Vegas slots, or into grandchildren’s Christmas stockings.

In the bad news media, all we hear about is the shortage of M2 in the Fed’s tightening cycle, but M2 is still $1 trillion above its pre-pandemic trendline, and demand deposits (mostly checking accounts) are $2 trillion above the pre-pandemic trendline. The sum total of all bank deposits plus money market mutual funds (MMMF) hit a record $22.8 trillion in 2022 and is still $2 trillion above its pre-pandemic trendline, and Baby Boomers hold $2.5 trillion more than they did at the end of 2019, before the pandemic struck. (Corporations also have a boatload of cash. Corporate cash flow hit a record high at the end of 2022.)

Those still working also have a lot more disposable cash, and – as Ed Yardni likes to say – “Consumers are still doing what they do best.” They shop! He says that those who doubt Consumer Power should observe that “both inflation-adjusted wages and total disposable income have been rising again in recent months after mostly stagnating during 2021 and 2022. Real average hourly earnings rose 1.5% over the past 11 months through May.” He adds that, “Consumers also have other sources of record unearned income including (during May, at a seasonally adjusted annual rate): proprietor’s income ($1.9 trillion), interest income ($1.8 trillion), dividend income ($1.7 trillion), Social Security benefits ($1.4 trillion), and rental income ($0.9 trillion). May’s total was $7.7 trillion, equivalent to 65% of wages and salaries.”

Yardeni also opines that “American consumers spend money when they are happy and spend even more money when they are depressed,” something akin to alcoholics who either celebrate or drink in sorrow.

“They’ve been going shopping to release some dopamine in their brains to make themselves feel better.”

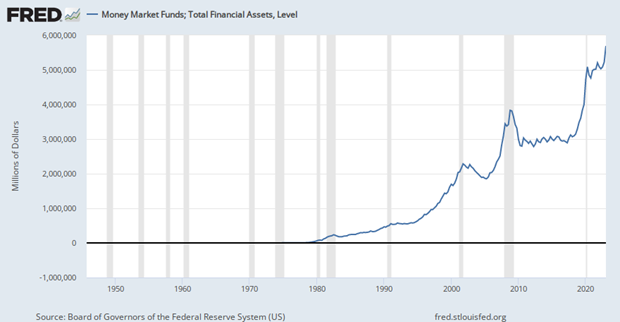

No Recession (or Market Crash) is Likely with Record-High Cash on the Sidelines

The payoff for investors is that there is little likelihood of a market crash – or a steep correction – with such a record amount of cash on the sidelines, including a record $5.7 trillion in Money Market Funds.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

With consumers purchasing goods and services, to get that dopamine fix, a holiday season approaching, and with investors rushing back into stocks for Fear of Missing Out (FOMO), there is little likelihood of a necessary recession (“hard landing”) to cure inflation. Ed Yardeni calls this “The Case for Immaculate Disinflation,” that inflation will be slowly cured by Fed policies returning to normal with no necessity of some moonshot to 6% or higher on the Fed Funds rate to fight phantom “permanently high” inflation, the same way they mistakenly ignored the early inflation onset for a full year, falsely calling it “transitory.”

It turns out that the Consumer Price Index was indeed “transitory,” but only after the Fed acted to treat the disease with respect instead of ignoring it. Once they raised rates and cut off QE, inflation peaked (in June 2022) almost immediately and began falling. The Fed waited far too long to act, but they finally wised up.

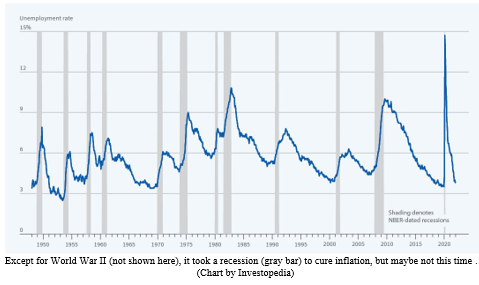

Economic historians say the only way to bring down high inflation is with a recession. In the last century, the only exception was in the 1940s, during and after World War II. Well, streaks are made to be broken.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

This could be the only time since World War II when inflation will be cured without a recession, since the pandemic was also a unique historical outlier, just like World War II was. The pandemic recession was an entirely man-made creation, through lockdowns – and so was the “helicopter money” inflation that came during the lockdown year (2020) and the Biden series of benefits, checks, and high-spending bills in 2021. The Fed was in charge of the morning-after hangover pill. It hurt for a while, but the medicine is working.

Now that our heads are presumably clearer, we are left with hefty personal bank and brokerage accounts. This should prevent the onset of that once-thought-certain recession or the much-anticipated market crash.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

China is “Losing its Mojo” Under Dictator-for-Life, Xi Jinping

Income Mail by Bryan Perry

A Rally in The Energy Sector Is Taking Shape

Growth Mail by Gary Alexander

Huge Boomer Assets Should Fuel More Market Growth

Global Mail by Ivan Martchev

The Broad Market Finds its Pulse

Sector Spotlight by Jason Bodner

Record Cash on Sidelines Says Millions Missed this Rally

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20 years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.