by Gary Alexander

May 9, 2023

While S&P 500 corporations are completing the task of submitting the unforgiving facts of their first-quarter top-line sales revenues and bottom-line earnings and profits, governments know their shareholders are helpless to sell stock in their nation, so they routinely publish scarlet red ink while living in what this week’s Economist labels “Fiscal Fantasyland.” Their forward guidance, if any, is to raise the debt ceiling.

Every day, the federal deficit hits a new all-time high, now approaching $32 trillion. Treasury Secretary Janet Yellen has set a “drop dead” date of June 1 for when the U.S. may renege on its debt payments, if we don’t raise the debt ceiling, so prepare for a month of dramatic accusations and blame-mongering.

We could service that debt with consistent GDP growth of 4% or more, but the Biden Administration and Federal Reserve have done everything in their power to slow growth to an anemic 1% pace as far as the eye can see. In an April 24, 2023 Wall Street Journal editorial, former chairman of the Senate Banking Committee Phil Gramm and former ranking member of the Senate Banking committee Pat Toomey, said:

“In the short term, President Biden’s regulatory tsunami will fuel inflation and make a recession more likely. In the long term, it could smother America’s productivity, wages and living standards. If the U.S. puts on a European-style rules straitjacket, American economic exceptionalism will perish.”

We’ve seen this movie before, most notably the Gingrich vs. Clinton ‘High Noon’ moments of 1995, and Obama vs. Tea Party Republicans in 2011 and 2013. We can learn lessons from these past encounters.

- 1995: After the Republican Revolution of 1994, the new House Speaker Newt Gingrich cut funding for favorite Democratic spending programs, resulting in a government shutdown from November 14 to 19, 1995, then from December 16, 1995, to January 6, 1996. The market took Doomsday in stride, rising 1.3% in the first 5-day span, and then +0.1% in the 21-day hiatus. In the longer run, the S&P 500 rose 34.1% for all of 1995 and another 20.3% in 1996. In the six years with President Clinton and a Republican Congress (1995-2000) the S&P 500 rose by 188%, including the dot-com bubble crash.

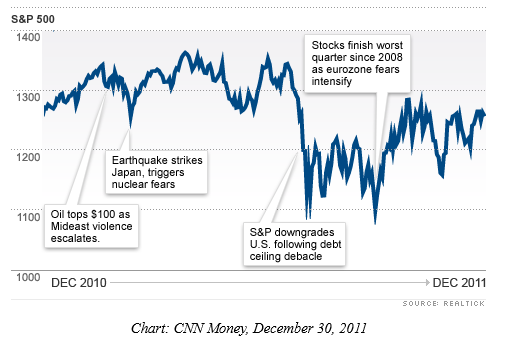

- August 2011 & October 2013: Since 1996, the only government shutdown lasting over three days was October 1-17, 2013, in the Obama era. In that instance, the S&P 500 almost rejoiced – rising by 3.1% in those 17 days – so it seems that these shutdowns do not spook the stock markets. But … any prolonged debt ceiling debate, or any downgrade of the U.S. credit rating is a different story. During August 2011, S&P downgraded the Treasury’s credit rating, which sent the S&P 500 into a tailspin.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

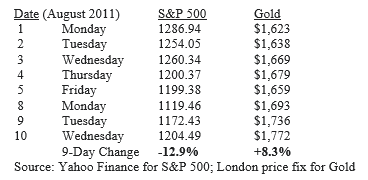

In early August 2011, gold soared after S&P downgraded the credit rating of U.S. Treasury debt – all coming during the debt ceiling debate. From $1,495 on July 4, gold rose 27% to $1,895 on Labor Day.

In the first 10 days of August 2011, gold rose 8.3%, while the S&P 500 declined by nearly 13%.

This brings us to “Gresham’s Law” – or why gold tends to rise whenever the dollar or stocks fall.

How Gresham’s Law Works Today – Examples from 1965 & 2011

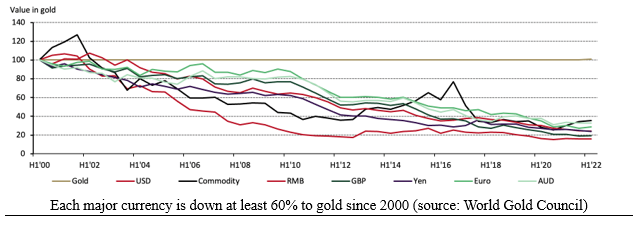

Gresham’s Law says that “bad money drives out good.” Thomas Gresham didn’t invent this law, but he was the monetary advisor in the early years of Queen Elizabeth I, so the principle is at least 450 years old.

In Gresham’s day, bad money usually meant a coin debased through clipping off some of its weight, or by using base metals. Over the last 20, 50, or 100 years, most currencies have lost most of their purchasing power to gold. Here is how the dollar, yuan, pound, yen, euro, and Australian dollar have fared since Y2K:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

A modern example of Gresham’s law was U.S. silver coinage in 1965 after President Johnson removed most of the silver content in favor of a copper sandwich in the 40% silver Kennedy Half-Dollar. All of a sudden, customers would pocket the old 90% silver coin and spend the 40% silver coin, and that big old bully LBJ couldn’t stop them with his warning on the day of this Great Silver Swap, on July 23, 1965:

“If anybody has any idea of hoarding our silver coins, let me say this. Treasury has a lot of silver on hand, and it can be, and it will be, used to keep the price of silver in line with its value in our present silver coin. There will be no profit in holding them out of circulation for the value of their silver content.” – LBJ.

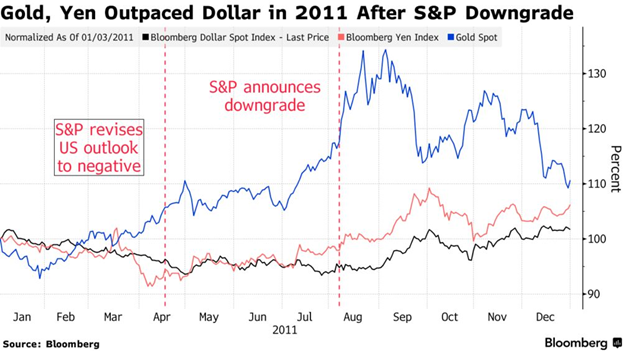

He was wrong. Silver gained 65% in three years, tripled in a decade, and gained 40-fold by 1980. Now, here is Gresham’s Law in action in 2011 as gold (blue line) soared when S&P downgraded dollar debt:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

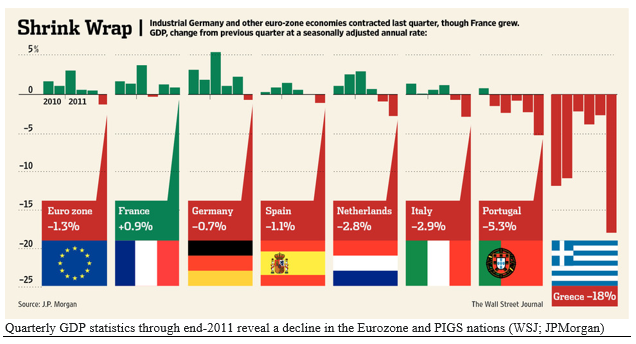

However, there was a sunrise in September. The U.S. economy never suffered a recession throughout all this drama. We went without a recession for a record 11 years, until COVID hit in 2020, but Europe was not so lucky. Due to their own bank problems and underperforming PIGS (Portugal, Italy, Greece, and Spain), the Euro-zone suffered negative growth in 2011, despite a weak dollar. Europe fell behind the U.S. in growth, stock market performance, employment statistics, and other metrics over the last decade.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

There is a parallel today. The U.S. may seem bad off in 2023, but not compared to other continents:

The Economist’s May 4 cover article says the debt crisis is global: “Those in Europe are locked in a silly debate about how to tweak debt rules, at a time when the European Central Bank is indirectly propping up the finances of its weakest members.’ Meanwhile, economist Ed Yardeni writes, “Parisian bakers report that their electric bills have quadrupled since Russia invaded Ukraine, while the costs of flour, butter, and eggs all are up about 50%.” Barron’s adds: “The headwinds facing boulangeries in France’s capital highlight why the European Central Bank is facing a tougher struggle than the Federal Reserve.”

China’s debt figures are hidden and harder to prove, but their centralized government has buried their bad decisions in a series of doubled-down bad bets in real estate, bad banks, overseas expansion, COVID shutdown protocols, and military saber-rattling in their region. They also are trying to rescue their weakest provinces, just like Europe did with their “PIGS” a decade ago. The Economist wrote this week (in “China’s local-debt crisis is about to get nasty”) that Beijing is pouring lots of money into Guizhou, their poorest province – a place where 32 subscribers to one of my previous global newsletter affiliations visited back in 1996, when many of us commented on the many empty buildings popping up in Guiyang.

Now, the Economist writes: “Over the past decade Guizhou, the region in which Guiyang sits, has accrued enormous debts through its building efforts—ones which it can no longer repay. Many of the region’s roads and bridges went untraveled over the past three years as covid-19 stopped people moving about. A local bridge-builder was recently forced to extend maturities on its bonds by up to 20 years. The region is also known for its shantytowns. Guiyang is scattered with skyscrapers and green hills poking out from between them, as well as old, crumbling buildings.”

So, when you see the debt ceiling debate escalate in the next month, keep your eyes above the fray and keep asking: Which nation looks best? The U.S. will likely be #1, and gold will still trump paper.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

Employment Reports & ISM Numbers Reflect a Growing Economy

Income Mail by Bryan Perry

Some Beaten Down REIT Subsectors Deserve a Closer Look

Growth Mail by Gary Alexander

When Gresham’s Law Meets a Debt Ceiling, Gold Can Soar

Global Mail by Ivan Martchev

If Bank Stocks Can Rally, the Market Can Rally Some More

Sector Spotlight by Jason Bodner

Some Takeaways from Chairman Powell’s Mid-Week Musings

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20 years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.