by Gary Alexander

February 6, 2024

President’s Day is officially the third Monday in February, marking the midpoint between two older holidays – Lincoln’s Birthday (February 12, 1809) and Washington’s Birthday (February 23, 1732), but today also marks the birthday of another great president, Ronald Reagan, born February 6, 1911. In fact, I would argue that these were the three greatest U.S. presidents of the 18th, 19th and 20th centuries.

Reagan’s official biographer, Edmund Morris, made a hash of the Gipper’s life, admitting that he didn’t understand his affable subject, but he began his bio, “Dutch,” with a touch of the actor’s dramatic flair:

“At 4:16 am on February 6, 1911, Ronald Wilson Reagan was born feet first, after 24 hours labor. Even in the womb, it seems, he plotted his entrance with dramatic effect. He weighed 10 pounds.” – Dutch, p. 14.

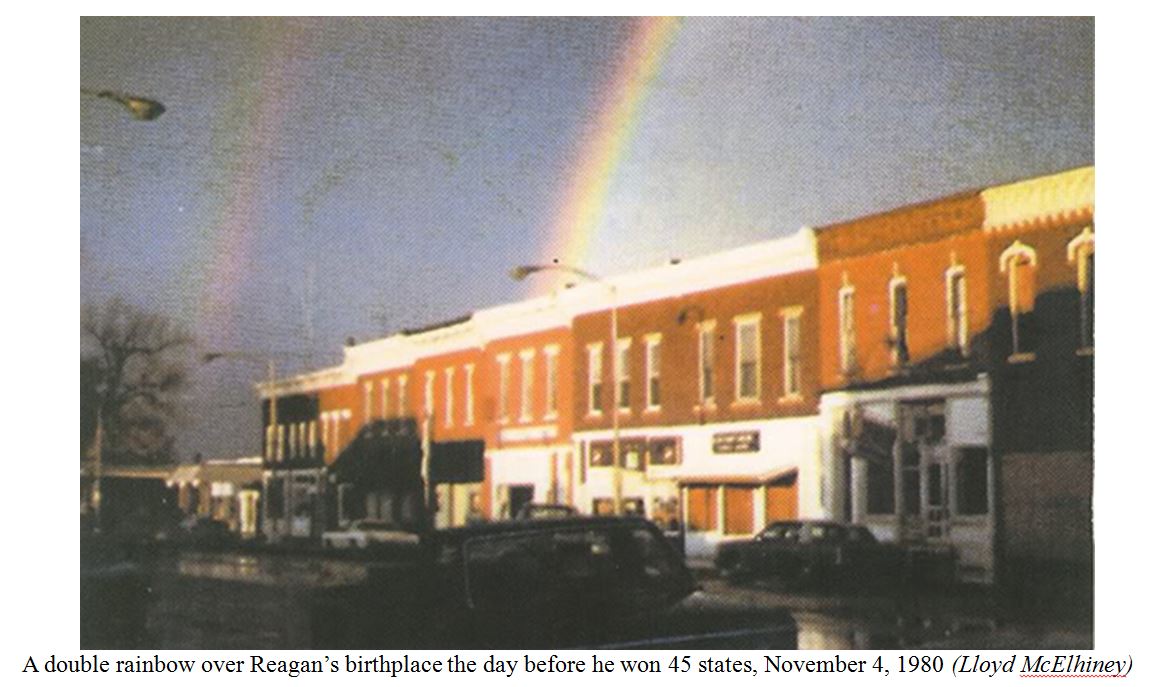

Reagan was born in Tampico, Illinois, the second and final son of Jack and Nelle Reagan. If you take this fairy tale seven decades forward, on the day before his 1980 election victory, the house where Reagan was born had become the First National Bank of Tampico. It was a rainy Monday, but as the rain lifted, a rare double rainbow appeared over the address where Reagan was born. Lloyd McElhiney, manager of the local grain elevator, ran home, hoping the image would last, grabbed his camera, and caught this image:

What Presidents (Since 1974) Were Best for Stocks?

When it comes to stock market performance, it’s easy to give most (or all) of the credit to the president or the party in power. They can help or hinder the health of the economy, but in the end, corporations are still the source of stock market earnings and profits, not politicians. The reigning tax policies and regulations can either hurt business or free businesses to compete, and Congress as well as the President’s rhetoric can give those businesses a clear path, or a barrier to profit. A President cannot fight a hostile Congress.

In that regard, it’s important to recognize that the Democrats controlled the House of Representatives for 40 consecutive years, 1954-94, including all of Ronald Reagan’s years in office, and the Democrats also controlled the Senate every year from 1954 to 1980, and 62 of the 82 years from 1933 through 2014.

With that caveat in mind, here is the performance of the eight elected Presidents of the last 50 years, as calculated from the date of their Inauguration Day, divided into two-term Presidents and one-term leaders.

Best Two-Term Presidents (in Terms of Stock Market Gains) Since 1974

A quick scan of these lists shows that Democratic presidents did better in two terms, Republicans in one term, but you must factor in the role of Congress. The real story is that the stock market tends to do best when the powers are split between the presidency and Congress. When Republicans controlled everything under George W. Bush from 2001 to 2006, the market went down, then crashed in his final year; and when Democrats controlled everything under Jimmy Carter, the market went down in real (after-inflation) terms. But when the powers were split, the market became supercharged. This is best illustrated by the times when there were even divisions – or mid-term course corrections – during these four presidencies:

Example #1: During Ronald Reagan’s years, the Democrats controlled the House all eight years, and they controlled the Senate in his final two years. Although House Speaker Tip O’Neill was noted for working well with the President in negotiating compromise, neither party got all they wanted, which kept either party from gaining total power. That trend continued during George H.W. Bush’s single term:

Example #2 is the most informative: Bill Clinton’s 8-year term is the blue-ribbon winner, but it’s a tale of two party dynamics. In his first two years, the S&P gained only 8%, when the House was massively (258 to 176) Democratic, along with a Democratic Senate – a blue state monopoly. Then came the Republican Revolution of November 2, 1994, when the Republicans gained 108 seats, from an 82-seat minority party to a 26-seat majority. The Senate also turned red in 1994. Both houses stayed red for the next six years.

The difference was reflected in the stock market, the economy and balanced budgets in 1998-2001. With a split Congress, the S&P gained 205% in six years, versus 8% in two years with a one-party monopoly:

Example #3 is staring us right in the face: The Biden years. During his first two years, President Biden had the same kind of one-party monopoly that Presidents Clinton, G.W. Bush, Obama and Trump enjoyed, and it apparently went to his head – just as it did to the four fellas I just named. Biden went too far in his ambitious spending plans, as did most of those others I just named (two from each party, please note).

The market reflects the same story – no market gains during Biden’s first two years, then spectacular gains the last year and three months, since the Republicans took over a modest majority in the House:

Once again, split power in government is better for investors than one-party monopoly of either stripe.

Let this be a lesson for how to plan your investments after the results come clear next November 5, 2024.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

The Latest Economic Data May Postpone Rate Cut Expectations

Income Mail by Bryan Perry

Hot Jobs Report Runs Counter to Soft ADP Data

Growth Mail by Gary Alexander

“President’s Month” Invites Presidential Comparisons

Global Mail by Ivan Martchev

Bonds Are Once Again More Volatile Than Stocks

Sector Spotlight by Jason Bodner

When You Can’t Find Good Answers…Create Your Own

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20 years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.