by Gary Alexander

December 19, 2023

This marks the sixth edition of my year-end column of “10 best books,” which began as a Christmas list of books for my college-age grandchildren in 2018. I gave them the write-up and enough money to buy the books. Who knows where the money went, but I decided to turn books into an annual event here.

As I wrote in 2018: “One of the keys to becoming a successful investor is to realize that the strongest long-term trends will always transcend the ebb and flow of daily market gyrations and scary headlines. The media will forever focus on the worst-case scenario, but the one thing I would counsel investors to remember is that seven billion people are working every day to make their life better, and that will always be a bullish force. … As you can see from these titles, I’m partial to books that cover a large historical canvas with a point of view that ties these great ideas together. I’ll profile them briefly here…”

Not much has changed since 2018, despite COVID and Trump versus Biden. If I gave you 10 books on trading, investing and economics alone, that would result in a narrow worldview. We live in a complex world. I read an average of 120 books a year – 10 a month – on a wide variety of subjects since 1965 or so, and this wide-ranging view of the changing world has delivered valuable investment insights for me.

Here are my 10 best books published during the last eight months, in publication order:

Book #1 is a tie: “Generations: The Real Differences Between Gen Z, Millennials, Gen X, Boomers and Silents – and What They Mean for America’s Future,” by Jean M. Twenge (published April 25; 560 pages) and “Generation Why: How Boomers Can Lead and Learn from Millennial and Gen Z” by Karl Moore (May 1, 216 p). Both are PhDs. Dr. Moore is a kindred spirit (on an alumni Forum). I actually prefer his book as more of a practical business leader’s guide to working with Gen-Z employees, students (or your own kin), but Dr. Twenge’s book is deeper and more academic in the trail of tears left by all of our generations, beginning with us Silents (born (1925-45), then the Boomers (1946-64), Gen X (1965-79), Millennials (1980-94), Gen Z (1995-2012) and the newborn “Polars” (born 2013-29). I think Twenge over-stresses the dominance of technology in Gen Z’s hands (and thumbs), whereas Dr. Moore has taught thousands of them, taken hundreds of them on global tours, and interviewed over 750 C-Suite executives on dealing with those under 40, so life is more than tech addiction. It’s about how to find meaning in life. Moore covers managing and working with younger people, bridging the gap between the old and young.

#2: “Best Things First: The 12 Most Efficient Solutions for the World’s Poorest and our Global SDG Promises,” by Bjorn Lomborg (May 8, 314p), where SDG means Sustainable Development Goals. Too many climate zealots take a closed-minded view, projecting current trends into a mathematical model – a method that has seldom worked in the past. Trends reverse, even with the climate, in ways scientists and others cannot see in advance. Lomborg argues that there’s no sense in impoverishing mankind based on unproven theories, ignoring economic trade-offs. Lomborg takes a welcome multi-disciplinary approach, saying that there are “at least 12 more efficient solutions for the world’s poorest people” than the UN’s SDG consensus. For instance, he argues that for about $35 billion a year—barely half of what the U.S. spends each year on humanitarian aid—these 12 policies could save 4.2 million lives and generate an extra $1.1 trillion in value every year, while the trillions spent on alternative energy save almost no lives.

#3: “Why Congress” by Philip A. Wallach (May 30, 336p) – note: There’s no question mark, no subtitle – but this book deserves both. The current political rancor and disrespect of Congress didn’t begin recently. I’d say it began in the 1790s, but Wallach targets the 1970s, when reformers delegated king-like powers to subcommittees, based on seniority, encouraging divisions. Barton Swaim and Yuval Levin, two other fine political writers, call this the “best political book of the year” (Swaim) and “the book that taught me the most this year” (Levin). Levin adds that “it should be mandatory reading for every friend of the American republic.” My view: We should not blindly assume our system is the best. It’s broken. This fine, thoughtful, non-partisan book is heavy on solutions, rather than rehashing all-too-obvious problems.

#4: “Broken Money: Why Our Financial System is Failing Us and How We Can Make It Better,” by Lyn Alden (August 20, 538p) covers the macro-history of money and banking with a focus on the failure of nearly all forms of paper money (and banking) and the eternal lure of gold. For instance, she writes, “The pound sterling of the UK is the world’s oldest continuously used currency that is still in use today. In Anglo-Saxon England during the eighth century, the pound sterling was defined as a pound of silver… Today a pound sterling is worth less than two grams of silver” (page 102). She also spoke of various failed currencies at the New Orleans Investment Conference in November, where I heard her speak.

#5: “Social Justice Fallacies” by Tom Sowell (September 19, 224 pages). Mostly, I’m delighted that this 93-year-old economic giant has retracted his announced retirement (I knew he would) to pen yet another tour de force on the failure of another aspect of the reigning zeitgeist – on his Stanford campus and beyond. One of my fellow economic writers penned a scathing review of Sowell recently, saying he is a flawed economist. I answered that he is more than an economist – he is a gifted demographer, geographer, race and ethnic analyst, behavioral analyst, and money and credit theorist: He is a basic Renaissance Man. He won’t waste pages on econometric models when he can drop gems of wisdom into each paragraph.

#6: “The Cancelling of the American Mind” by Greg Lukianoff and Ricki Schlott (October 17, 464 p): The McCarthy lasted about five years, but our cancel culture has already lasted almost twice that long, and it has destroyed about twice as many careers as McCarthy did, while spreading the same kind of witless fear and self-censorship, according to co-authors Greg Lukianoff (co-author with Jonathan Haidt of 2018’s “Coddling of the American Mind”) and Ricki Schlott, a recent college graduate who tried to turn the tide of censorship on her campus, to no avail. It strikes me as odd that our major media often hark back to McCarthy’s in movies, plays and TV shows while playing a leading role in doing the same today.

Three Visionary Geeks (and Mercurial Bosses)

Here are three gentlemen that likely sport genius-level IQ – but I wouldn’t want to work for any of them

#7: “Elon Musk,” by Walter Isaacson (September 12, 688p) is the pick of this trio, especially for Musk’s creativity and market power, but he grew up under an abusive father in South Africa, and that emerges in how he treats key workers, according to this inside view from ace biographer Isaacson (who also profiled Steve Jobs and Kissinger, among others). We’ll alwamanding 24/7 sweat and creativity, while breaking rules as a matter of course. We’ll never know why he bought Twitter (X), but we have lots of time to marvel at the rest of this dynamo’s life, since he’s only 52 and shows no sign of slowing down.

#8: “Going Infinite: The Rise and Fall of a New Tycoon,” by Michael Lewis (October 3, 288p) is a rollicking good profile of Sam Bankman-Fried, a similarly high-IQ creative kid who never really grew up, only in this case he is no Elon Musk: He never invented anything of value, even though he fooled the intelligentsia and glitterati of academia, Hollywood and Washington DC into thinking he was the Albert Einstein (or is it Isaac Newton?) of crypto-currency commerce and banking. In the end, he was nothing but another Ponzi-scheme-Madoff financial rip-off artist, funneling deposits to his girlfriend’s accounts to speculate on stocks and lose billions for some of those very famous names who revered him. Michael Lewis always delivers the goods – with telling anecdotes and colorful stories transcribed on the spot.

#9: “The Greatest Capitalist Who Ever Lived: Tom Watson Jr. and the Epic Story of How IBM Created the Digital Age,” by Ralph Watson McElvenny and Marc Wortman (October 24, 592) is a mis-titled book, perhaps out of family loyalty, since it is co-authored by a member of the founding family of IBM. The book bares the flaws and failures of Thomas Watson, Sr. and Jr., and their dysfunctional family. As for “greatest capitalist,” sorry, he’s not in the Top 10, in my book: IBM relied too heavily on government aid, so it can hardly be the “greatest capitalist” story. Watson himself didn’t even want to enter the family business at first; he preferred flying and sailing. I can think of at least half dozen better capitalists off the top of my head, like John D. Rockefeller, Cornelius Vanderbilt, James J. Hill, Bill Boeing, Henry Ford, Alfred Sloan of GM, Steve Jobs and Bill Gates, who later brought IBM to its knees, but this is still a gem of a read about one tortured man, his family and the big risks he took to dominate a complex industry.

The Book of the Year: Milton Friedman’s Long-Awaited Intellectual Biography

I’ve saved the best for last. It’s about time somebody treated Uncle Miltie with some deserved respect:

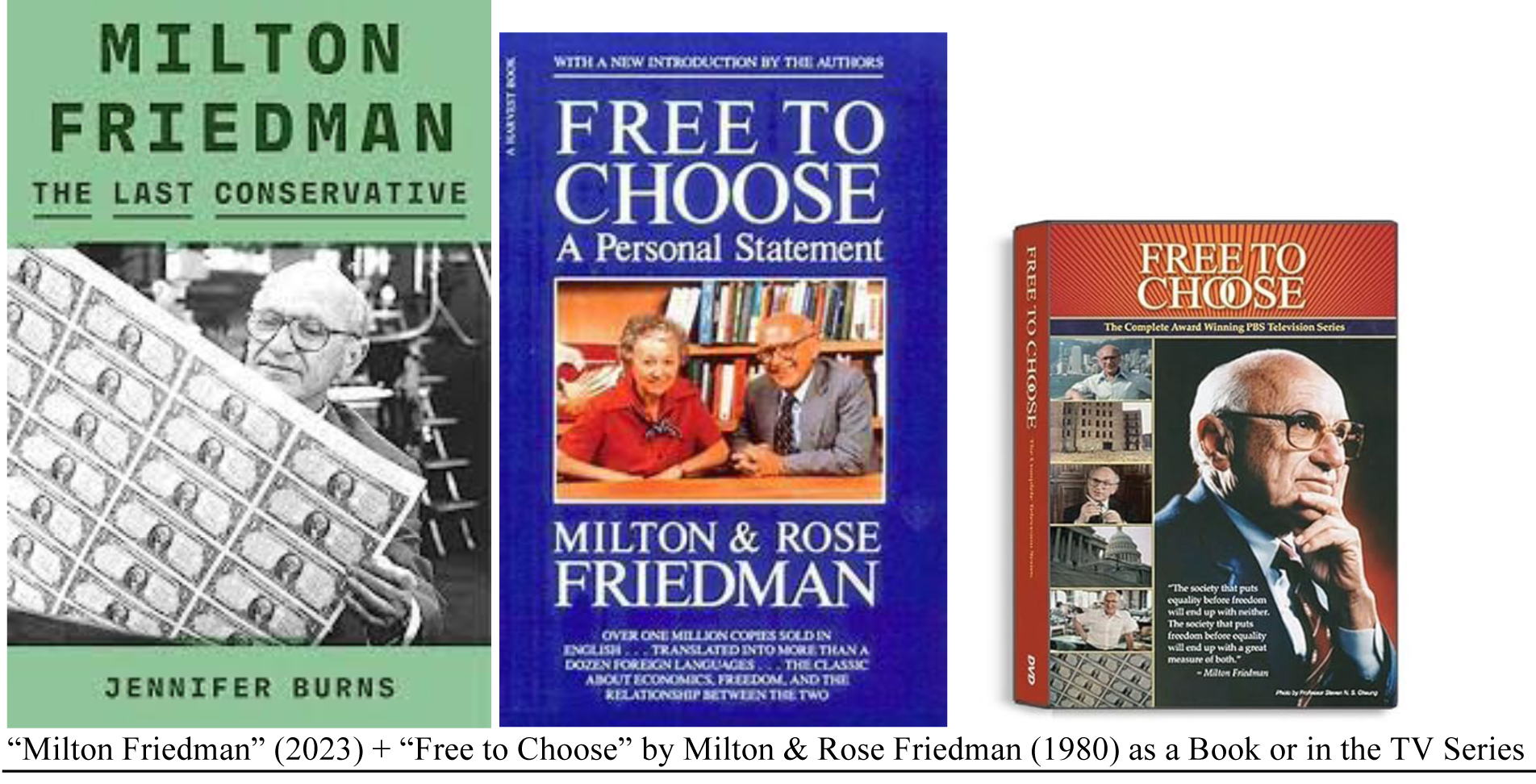

#10: “Milton Friedman: The Last Conservative” by Jennifer Burns (November 14, 592p) covers the top economist of the 20th century, in my view. I first read his views in Newsweek in the 1960s and 1970s but my first big exposure to his work in detail was in his 10-part “Free to Choose” TV series in 1980, which everyone should rent or see on tape, or read (below). Thomas Sowell was also a star in that series.

I had the honor to interview Friedman three times (once along with his economist wife Rose) from the 1980s to early 2000s in conjunction with the New Orleans Investment conference. He was always witty as well as wise against any trick questions. (Woe be to anyone who thought otherwise.) This is a biography of his thoughts, my favorite kind of bio. I’m learning a lot about his youth and early years. I’m not through yet, as I’m savoring every page, but it has already earned top marks of the 10 books profiled here.

In closing, here’s a link to one of my three interviews with Dr. Friedman, this one from the late 1998 New Orleans Investment Conference. Friedman speaks for the first 32 minutes, then I interviewed him for the last 25 minutes. I’m sharing it here because I think it is worth seeing how sharp his mind was at age 86.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

Chairman Powell Confirms That Inflation is Near His Target 2%

Income Mail by Bryan Perry

New Bull Market for Regional Banks? Not So Fast

Growth Mail by Gary Alexander

My 10 Best Books of 2023 (Christmas Gift Ideas)

Global Mail by Ivan Martchev

Fed Chair Jerome Powell Goes Full Circle

Sector Spotlight by Jason Bodner

Long (and Super-Short) Cycles in Nature and in Markets

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20 years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.