by Gary Alexander

October 3, 2023

It happens often in sports – most recently when a woeful 1-3 Baylor team, on the road at favored Central Florida (3-1), trailed 7-35 late in the third quarter, but then scored 29 points in the fourth quarter to win 36-35. The previous week, my beloved New Orleans Saints (NFL) visited Green Bay. The Saints were Marchin’ in to a seeming victory in the final quarter, leading 17-0, when the announcer noted, “the last time the Packers trailed 17-0 at half-time, they rallied to win.” Sure enough, Green Bay won again, 18-17.

Who cares about a Hollywood writers’ strike when sports can deliver such unscripted dramas each week?

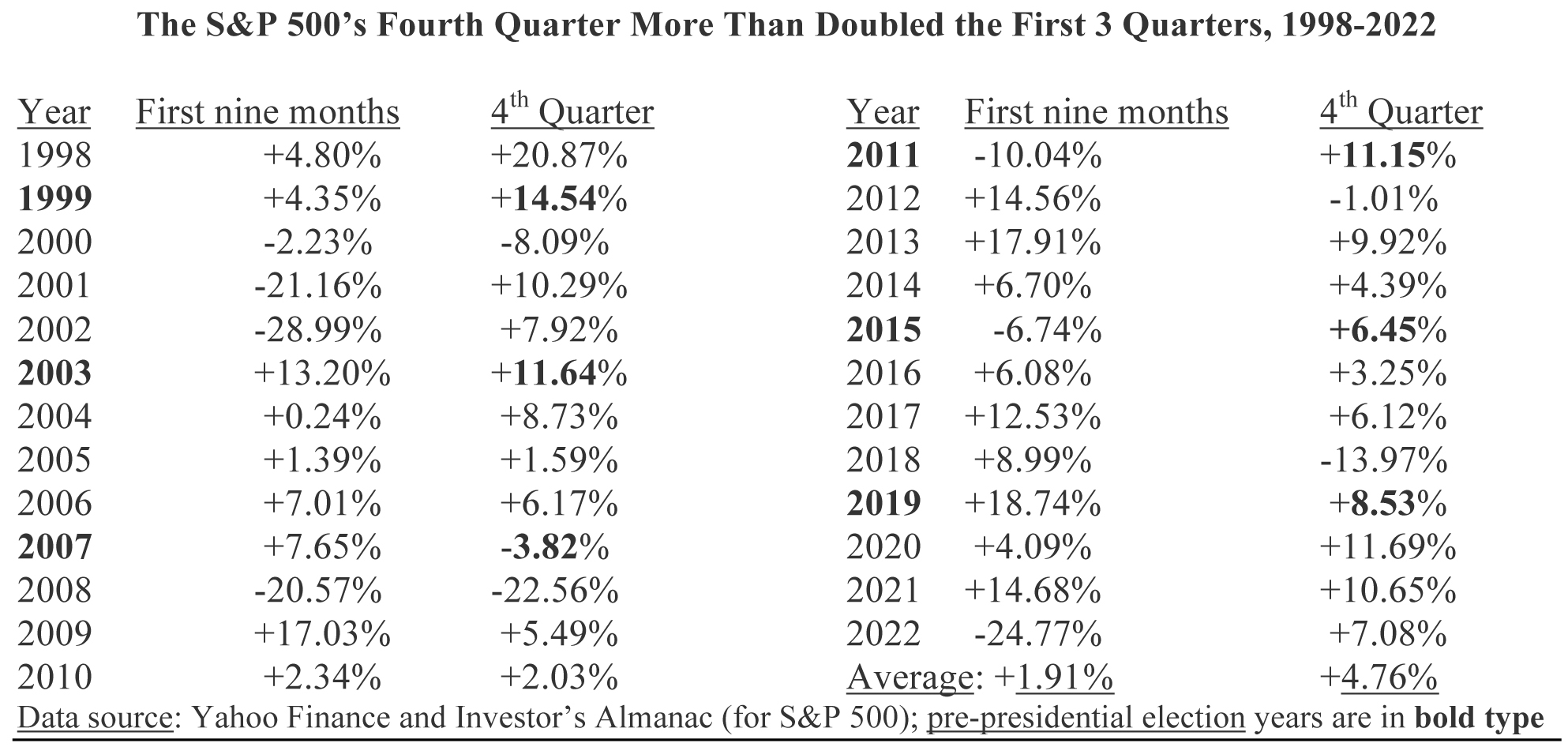

The stock market is something like these sporting tilts. The most significant action often happens in the fourth quarter. That doesn’t mean you can ignore the first three quarters. Those nine months provide the foundation for the fireworks to come, but you can’t argue with history, either. In the past 25 years, the fourth quarter has delivered more than twice the returns of the first three quarters: +4.67% vs. just 1.91%:

The S&P 500’s Fourth Quarter More Than Doubled the First 3 Quarters, 1998-2022

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

There were some exceptions, of course, but many times a dismal downdraft in the first nine months ended with a significantly positive fourth quarter, such as 2001, 2002, 2011, 2015 and, 2022, while the last six pre-presidential election year fourth quarters (like this year) were up 8.1%, on average.

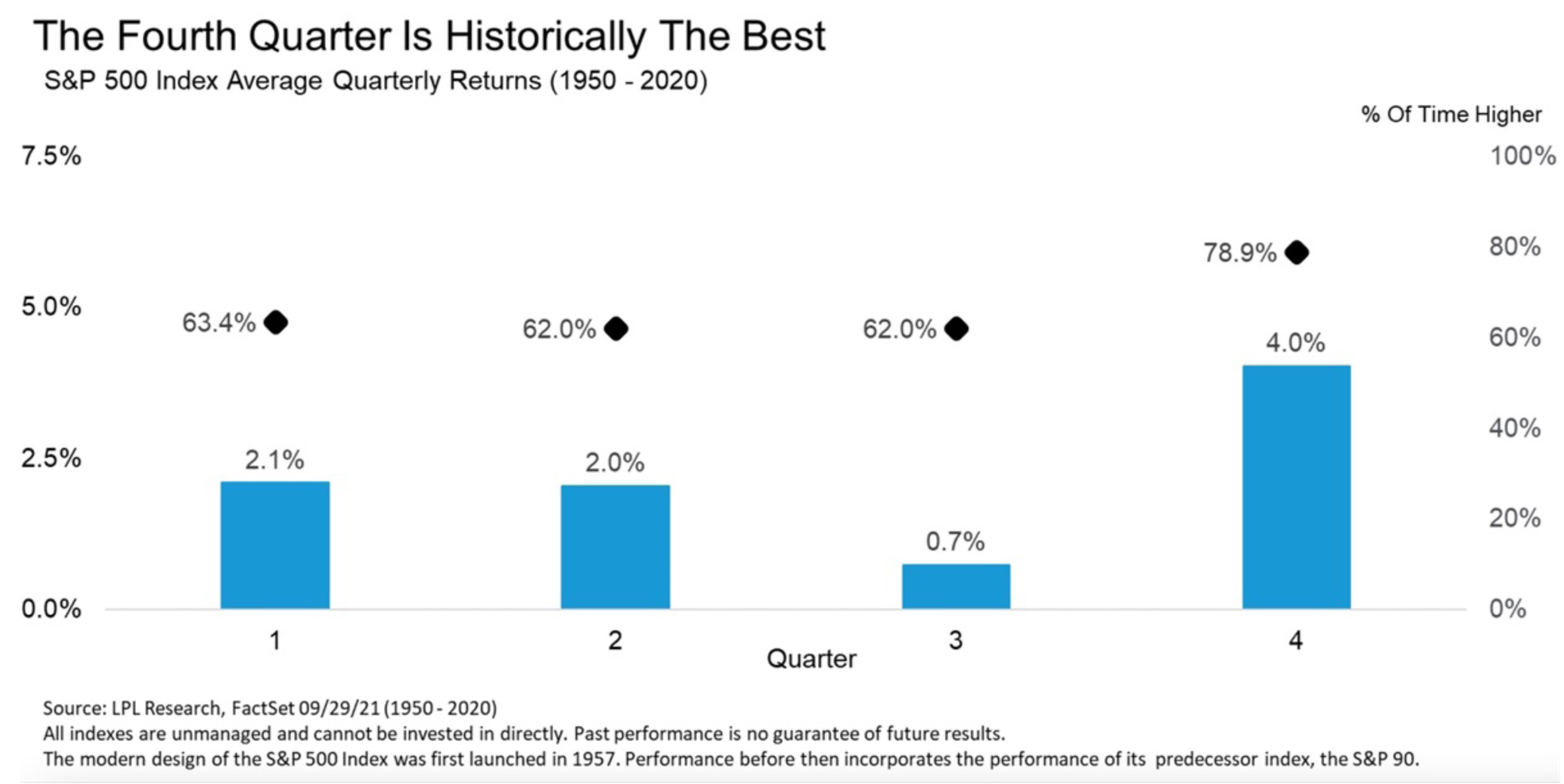

Going back to 1950, and skipping the great turnaround in 2022, the numbers aren’t quite so dramatic, but the fourth quarter still dominates the annual returns from 1950 to 2020, with the S&P 500 up 4% in the fourth quarter, but only 2.1%, 2.0% and 0.7% in each of the previous three quarters:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

What’s more, each of the three months in this quarter has developed a solid track record, even though October used to be the scariest month, due to memorable crashes in 1929 and 1987, plus a few other minor crashes in past Octobers. In recent decades, however, September has become the worst month.

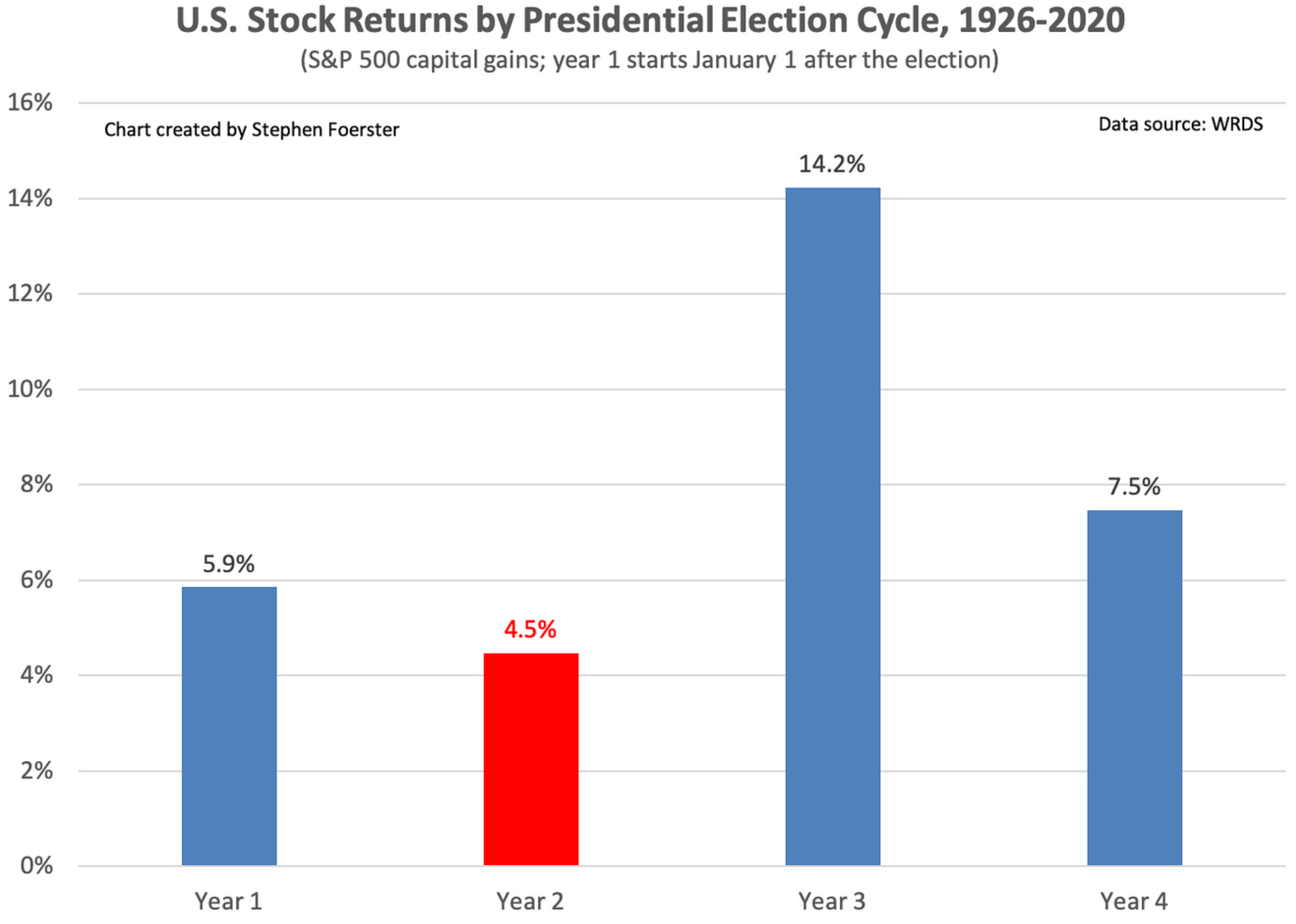

Since 1950, Pre-Election Years (Like This) Averaged 16.6% Gains

The bigger story is the performance of the market in pre-presidential election years as a whole. Since 1951, the 18 Presidential cycles have averaged +16.6% in the S&P 500, with only one slight downer in 2015, followed by a protean recovery in 2019, +29%. The fourth quarter, however, has not been so healthy, pre-1990, rising only 3.3% in the 18 cycles, brought down in large part by the crash of 1987.

When it comes to 2023, it’s a story of mixed index results, with the S&P 500 index being Goldilocks.

In the first nine months of 2023, the Dow Industrials and Russell 2000 were “too cold,” up only 1.1% and 1.35%, respectively. In contrast, the NASDAQ Composite was “too hot,” up 26.3% and the tech-rich NASDAQ 100 (QQQ) rose 35.1% through Friday, but the S&P 500 was in the middle, rising +11.7%. If 2023 comes up to the average of a 16.6% annual gain, we could see a modest 5% fourth-quarter gain.

Going back further, to 1928, the trend remains the same, though not quite up to the 16.6% since 1950:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Why the Big Surge in Most Fourth Quarters – And Will it Happen Again?

We can offer some technical reasons for fourth-quarter surges – such as pension-plan funding, tax buying or selling, and year-end fund window dressing – but Louis Navellier and I are convinced that one of the main engines driving fourth-quarter performance is the holiday season, sports, family get-togethers and looking forward to the New Year, especially if we can see some political relief ahead.

Thanksgiving and Christmas are the two most positive, family-oriented holidays on the calendar, and most people enjoy getting together to feast and watch a little football or other sports, and then toast the New Year with hopes for better times in America and in their stocks or portfolio performance.

This time around, we have the added attraction of a revival of earnings after a cyclical trough during the 2023 slow-growth “soft landing” engineered by the Federal Reserve’s interest rate-raising cycle.

Third-quarter earnings season is about to begin, but the market will be trading mostly on earnings guidance for the final quarter and the outlook for 2024. So far, analysts are optimistic about the S&P 500 companies’ prospects for 2024, forecasting (collectively) an 11.7% earnings increase in 2024, following a likely 1% gain when 2023 is fully accounted for, following a mediocre 7% gain in 2022.

According to economist Ed Yardeni and his team, earnings are currently expected to grow in all 11 S&P 500 sectors in 2024, led by the small-population Communication Services sector (+18.2%), then Technology (15.3%), Consumer Discretionary (+15.1%), Health Care (+13.1% and Industrials (+13.1%). Those are mostly the growth-oriented sectors within the S&P spectrum.

When it comes to industry sub-sectors, analysts (using Thomson Reuters I/B/E/S data), see top performance next year in movies and entertainment (+66%), publishing (+51%), property and casualty insurance (+47%), commodity chemicals (+40%), gold (+38%) and semiconductors (+37%). Among those sectors, stock indexes for insurance (-2%) and gold (-16.5%) are down year-to-date.

This is no guarantee of future performance, of course – and neither does any historical trend happen every year – but the folks at The Almanac Investor have shown that the four-year presidential cycle is a reliable historical trend, and fourth-quarter stock surges are much stronger this century than last.

Now, if only my NFL home teams (Seattle and New Orleans) can conquer their fourth-quarter jitters.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

Crude Oil Prices Reach a 13-Month High

Income Mail by Bryan Perry

Lower Inflation May Not Mean Lower Treasury Yields

Growth Mail by Gary Alexander

The Fourth Quarter Explosion is About to Start

Global Mail by Ivan Martchev

The Selloff in Stocks is the Fed’s Fault

Sector Spotlight by Jason Bodner

October – the Good News and the Bad News

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20 years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.