by Gary Alexander

June 6, 2023

David Malpass was appointed to a five-year term as head of the World Bank, but he will leave that office this month, early in his fifth year. I find it interesting that he resigned early not over criticisms of slow global growth – which would be his mandate – but over critiques about his climate knowledge.

All he did was claim that he was not a scientist. Sorry, David, that’s not good enough. In today’s world, even central bankers can’t keep their jobs if they hold nuanced views, like “some fossil fuels are cleaner than others.” (See: David Malpass: World Bank leader who was called climate denier quits – BBC News)

At any rate, Malpass wrote a valedictory address of sorts in The Wall Street Journal (“The World Needs to Get its Growth Back,” May 24, 2023), which opens: “The global economy is facing dangerously slow growth of 2% or lower. As I near the end of my term as World Bank president, I’m discouraged by the lack of resolve and action. I worry that slow growth may persist for years. The world is digesting the huge buildup of government debt relative to gross domestic product, normalization of artificially low interest rates, and a system allocating capital away from small businesses and toward bond issuers, especially governments and the largest businesses. The result is reduced dynamism at home and fragility abroad.”

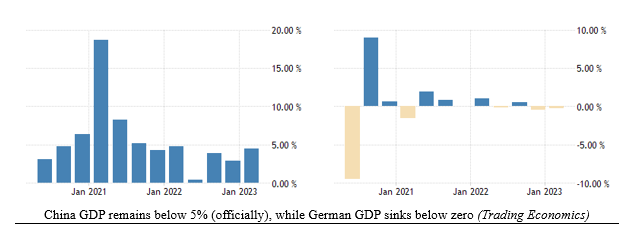

He’s right. The top three economies – The U.S., China, and Germany (tied with Japan at #3) – are being intentionally held back from their peak performance level by ideologues putting a series of weights on the backs of their premier performers – more so than usual, that is. According to an editorial in last Friday’s Wall Street Journal (“The Global Economic Growth Deficit”), #2 China is slumping, and #3 Germany is slipping into recession, while the U.S. is locked in a terminal slow-growth rut, while avoiding a recession.

In a nutshell, all three nations (and my home state) have succumbed to belief systems over economics:

- China’s “chairman for life,” Xi Jinping, seems to be a more devoted Communist than each of his four more pragmatic predecessors. While Deng Xiaoping famously said of communism vs. capitalism, “It doesn’t matter whether it is a yellow cat or a black cat, as long as it catches mice,” The Wall Street Journal reminded us that “Chinese President Xi Jinping is waging a campaign against the country’s private economy to maintain Communist Party political control. This includes regulatory crackdowns on tech companies that should be leading a rapid economic expansion.”

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

- Germany’s ideology is centered around green purity, after making a foolish “all in” bet on wind and solar power while ignoring the more secure non-fossil alternative of nuclear power. The Journal says, “Reality is also catching up with the German economy, which contracted 0.3% in the first three months of the year after shrinking 0.5% in the previous quarter, with consumer spending especially weak and inflation high. The surprise is that this didn’t happen sooner, given the burden of Berlin’s green-energy malinvestment and rising fossil-fuel prices after Russia invaded Ukraine.”

- The U.S. is the healthiest of the three, but not by much. We suffer from the Biden administration’s “hostility to affordable fossil fuels,” although not yet to Germany’s extreme, while adding a focus on “equity over growth” in “nearly all economic decisions.” The Journal further says that Mr. Biden is “using regulation to allocate private capital across the economy, often in unproductive ways.”

- In my home state, Washington, cement truck drivers willingly destroyed their company’s product, but the State Supreme Court upheld the Union’s right to sabotage their company. The U.S. Supreme Court reversed our state court’s ruling, but this is an example of the “unproductive ways” economic growth is sabotaged (see “Union Sabotage at the Supreme Court,” Wall Street Journal, June 2, 2023).

Where the Big 3 Economies Went Wrong

All three nations have been big growth engines for decades. Germany has been Europe’s top performer since the 1950s, overcoming the slower work habits in Mediterranean economies and work slowdowns in France and other socialist-leaning nations. China has been the miracle-working growth engine of Asia, since Japan went into slow-growth limbo in 1990, and the U.S. has been the world leader for a century.

China will continue to underperform for several reasons. One reason is their demographic destiny of fewer babies, meaning fewer workers supporting a growing army of older and retired parents needing aid. But in the immediate future, Chairman Xi (who must be obeyed) has declared that the traditionally corrupt and cossetted State-Owned Enterprises (SOEs), which were gradually being phased out by the previous three more practical CCP Chairmen, will be rewarded and encouraged from now on. Last November, Xi approved a new plan to make these SOEs “stronger, better and bigger,” to “optimize and restructure the state economy layout” – a euphemism for forced mergers – after Xi’s enforcers found that the SOEs were more obedient during Beijing’s forced COVID lockdowns and other strong-arm measures from the State.

Everyone expected China to come bursting out of the chute once their Covid lockdown ended, but it didn’t happen – and now we know why: The somnolent SOEs are in control. China sputtered and never took off this year. China just reported that its official purchasing managers’ index (PMI) for manufacturers contracted for the second straight month, and its services PMI declined almost two points to 54.5 in May.

So – 45 years after Deng Xiaoping began his first capitalist experiments in 1978, Xi is turning back the clock to Mao’s doctrinaire communism. Ideology has blinded him, and it will choke off China’s growth.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Germany suffers from a mass “green” mania, dreaming they could abandon all forms of fossil fuel and go “all in” on wind and solar for a growing economy. First, former Chancellor Angela Merkel shut down eight nuclear reactors in response to the 2011 Fukushima nuclear disaster – which was due to a tsunami, which poses no threat in Germany. Then she vowed to shut down all other nuclear facilities by 2022, although nuclear is a clean source of power. Then she vowed to build 25,000 megawatts of sea-based wind turbine power by 2030 and chew up almost 2% of Germany’s land for bird-killing wind turbines.

The German magazine Der Spiegel (The Mirror, pictured above) wrote back in May 2019, “Over the past five years alone, the ‘energy transition’ (Energiewende) cost Germany €32 billion ($36 billion) annually.” Der Spiegel cited an estimate that it would cost Germany “€3.4 trillion ($3.8 trillion),” or seven times more than it spent from 2000 to 2025, to increase solar and wind three to five-fold by 2050.

Michael Schellenberger responded, in Forbes: “If renewables can’t cheaply power Germany, one of the richest and most technologically advanced countries in the world, how could a developing nation like Kenya ever expect them to allow it to ‘leapfrog’ fossil fuels?” He cited the new wind farm in Kenya, inspired and financed by Germany and other well-meaning Western nations, which “is located on a major flight path of migratory birds. Scientists say it will kill hundreds of endangered eagles,” an added cost.

The U.S. isn’t as fanatic as many green zealots in Germany, but we’re close, as the Biden Administration seems determined to fulfill their fearless leader’s numerous campaign promises of “no more fossil fuels.” In one Presidential debate, Mr. Biden said, “No more drilling, including offshore. No ability for the oil industry to continue to drill, period,” making no exception for a relatively clean fossil fuel, natural gas.

In addition, the Biden Administration has added a major emphasis on “institutional diversity, equity and inclusion,” which is rife with opportunity for corruption and diversion from goals of growth into settling scores. After America resoundingly elected a black President, and then re-elected him, race relations were better than ever, but The New York Times decided in 2019 to focus on the fact that America is a racist nation, and the 1619 Project was their first manifesto to emphasize race; so major organizations must now focus on filling meaningless positions and balancing color codes instead of promoting economic growth.

It’s time for China to return to “capitalism with a Chinese face,” Germany to return to a balanced energy policy, and the United States to promote fairness with freedom once again, so we can all grow with vigor.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

“AI” Is Hot, But Don’t Get Burned

Income Mail by Bryan Perry

The Market Breaks Out as Debt Increases and Money Supply Decreases

Growth Mail by Gary Alexander

Ideology is Limiting Growth in the World’s Top 3 Economies

Global Mail by Ivan Martchev

Recession is Still Nowhere to be Seen

Sector Spotlight by Jason Bodner

How is Your Team (of Stocks) Doing?

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20 years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.