by Bryan Perry

January 21, 2026

As of last week, Kevin Warsh emerged as the front-runner to succeed Jerome Powell as Chairman of the Federal Reserve in May. His potential selection is a significant point of discussion for financial markets due to his unique blend of Wall Street experience and hawkish economic views.

Warsh was appointed to the Federal Reserve Board of Governors by President George W. Bush 20-years ago and was sworn in on February 24, 2006, at the age of 35, making him the youngest person appointed to the Board of Governors in the 112-year history of the Federal Reserve. Bush nominated him on January 27, 2006, to fill the unexpired term previously held by Ben Bernanke, who had just become Fed Chair.

At the time, his appointment was controversial due to his age and perceived lack of experience compared to typical Fed governors. However, he became a central figure during the 2008 financial crisis, serving as the Fed’s primary liaison to Wall Street and a key advisor to Chairman Bernanke. While appointed by Bush, Warsh continued to serve into the Barack Obama administration before resigning in March 2011.

Warsh’s leadership experience during the 2007-2009 financial crisis provides the best clues for how he might lead the Federal Reserve in 2026 and beyond. While only in his late thirties during the 2008 crisis, Warsh held an outsized influence then, surpassing many of his more senior colleagues on the Board.

Prior to his public service, he was an Executive Director at Morgan Stanley in Mergers and Acquisitions. Because of his background there, he was the Fed’s primary point-man with the CEOs of major investment banks. When the system began to freeze in 2008, Warsh was the person on the phone with terrified bank executives, translating the chaos of the trading floor for the academic-oriented economists at the Fed.

Warsh was a key architect in the forced take-overs and bailouts of 2008. He helped negotiate JPMorgan’s acquisition of Bear Stearns and was a central figure in the discussions surrounding the AIG bailout and the fateful decision to let Lehman Brothers fail. He spent a significant amount of time on Capitol Hill, selling the Fed’s emergency measures to skeptical Republicans, wary of government intervention.

Although he initially supported the emergency measures (like cutting rates to zero), Warsh eventually became one of the first and most vocal critics of the Fed’s long-term reliance on easy money. In 2010, he publicly broke with Ben Bernanke in a Wall Street Journal op-ed, questioning QE2, the second round of Quantitative Easing. He worried over printing money leading to inflation and “market distortions.”

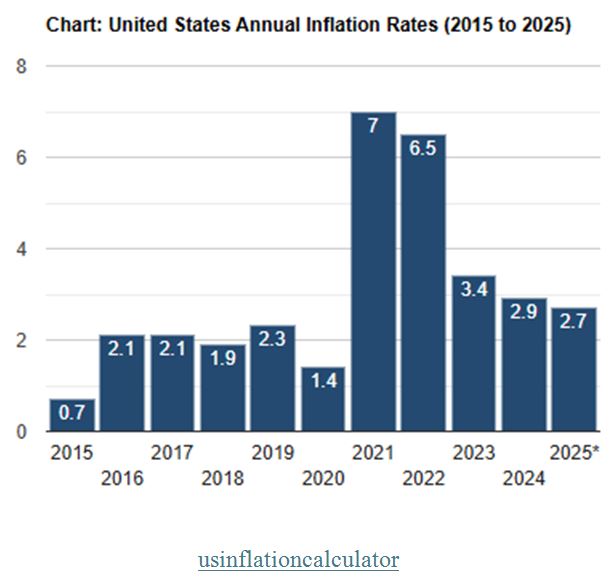

Warsh famously referred to Quantitative Easing as a “reverse Robin Hood” policy, as it benefited wealthy asset holders (stock and real estate owners) while doing little for the average Main Street worker. He resigned from the Fed in 2011, seven-years before his term was to expire, historically, Warsh is known as an inflation hawk, famously stating, “Inflation is a choice,” since price levels are driven by decisions of fiscal and monetary authorities rather than just external shocks. While traditionally hawkish, he recently expressed support for interest rate-cuts combined with aggressive balance sheet reduction (quantitative tightening). This “rate-cuts + QT” approach is a pragmatic compromise aligned with current political desires for lower rates while maintaining price stability.

If Warsh is confirmed as Chair this May, his past suggests a strategic reset. He has recently argued the Fed has “strayed from its remit.” He would likely prioritize shrinking the Fed’s balance sheet more aggressively. He prefers using market signals (like bond yields and commodity prices) to guide interest rates rather than relying solely on the Fed’s economic models, which often fail to predict inflation.

Warsh has proposed a strategy called Pragmatic Monetarism to help manage this burden. His plan focuses on a dual-track approach, of shrinking the Fed’s own balance sheet to lower the cost of the debt, rather than just the debt. Unlike some who want to raise the inflation target to 3%, Warsh remains a staunch advocate for a strict 2% (or lower) target, viewing price stability as the North Star for a healthy economy.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

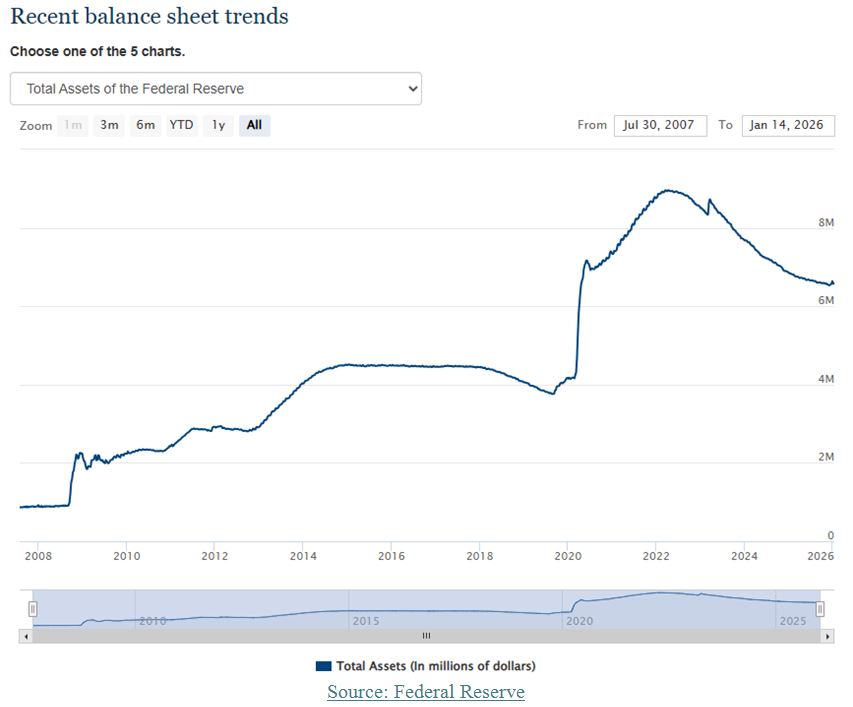

Warsh argues the Fed has practiced “fiscal dominance” in the last 15-years, by essentially keeping interest rates artificially low to make it easier for the government to borrow trillions. He wants to end the recent “printing press era.” He believes stopping the Fed’s massive purchase of government bonds can force a clearer separation between the Treasury (which spends) and the Fed (which manages money).

This is his most distinctive proposal. He says the Fed’s $7-trillion balance sheet is actually keeping interest rates higher than they need to be. He argues the policy of the Fed aggressively selling off its assets in the form of quantitative tightening “quiets the printing press.” Warsh further believes a smaller, more disciplined Fed balance sheet reduces inflation expectations so effectively the Fed can then lower interest rates for households and businesses without causing inflation to spike. Lower interest rates, in turn, can reduce the interest expense the government has to pay on its $38-trillion in red ink.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Warsh’s current activities include serving as the Shepard Family Distinguished Visiting Fellow in Economics at Stanford University’s Hoover Institution. He is also a lecturer and Dean’s Visiting Scholar, where he teaches and conducts research on economics and finance. He is on the Board of Directors of major firms, a partner at Duquesne Family Office, working alongside billionaire Stanley Druckenmiller. He is also a member of the Group of Thirty (G30), an international body of leading financiers and academics, and serves on the Panel of Economic Advisers for the Congressional Budget Office (CBO).

Based on his broad experience in financial crisis management, his understanding of Wall Street, his communication skills, as demonstrated on Capitol Hill, and his passion to reign in the $38-trillion debt and drive inflation lower, this puts Kevin Warsh squarely in the spotlight to be the next Fed Chairman.

Navellier & Associates; own JPMorgan Chase & Co. (JPM), in some managed accounts. Bryan Perry does not personally own JPMorgan Chase & Co. (JPM).

All content above represents the opinion of Bryan Perry of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

Is Another Regime Change Coming Soon – This Time in Iran?

Income Mail by Bryan Perry

Kevin Warsh Has the “Chops” To Be Our Next Fed Chair

Growth Mail by Gary Alexander

Trump 2.1 Shocks the Pessimistic Pundits

Global Mail by Ivan Martchev

The Great Rotation Continues

Sector Spotlight by Jason Bodner

The Market Surge May Be Signaling a Coming Explosion in Growth

View Full Archive

Read Past Issues Here

Bryan Perry

SENIOR DIRECTOR

Bryan Perry is a Senior Director with Navellier Private Client Group, advising and facilitating high net worth investors in the pursuit of their financial goals.

Bryan’s financial services career spanning the past three decades includes over 20-years of wealth management experience with Wall Street firms that include Bear Stearns, Lehman Brothers and Paine Webber, working with both retail and institutional clients. Bryan earned a B.A. in Political Science from Virginia Polytechnic Institute & State University and currently holds a Series 65 license. All content of “Income Mail” represents the opinion of Bryan Perry

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.