by Jason Bodner

July 8, 2025

“We suffer more in imagination than in reality.” – Seneca, the Roman Philosopher

This insight rings true across the centuries, and it continues to resonate today. People, as a rule, tend to worry about things that never actually happen. Our imaginations are powerful—sometimes too powerful. They can often create elaborate scenarios filled with fear, anxiety, or doubt. These scenarios rarely come to fruition, yet they shape our actions, mood, and decision-making in very real and sometimes costly ways.

That same lens of psychological insight applies to investing. I just heard from my dad, an accomplished investor. Calling him accomplished would be an understatement. Last week, I told you about our first meeting with Louis Navellier in his Reno corporate offices in the early 1990s, since dad wanted to see his operation up close and ask the team about their investing discipline before investing there. As a result of dad’s skills and Louie’s team, he has been living off his investment successes and skills for more than 20-years, managing his nest egg with consistency and focus. His investment accounts have continued to grow and compound handsomely. He’s seen market crashes come and go – booms, bubbles, and bear markets.

With that background, when he asked me a particular question last week, I knew it wasn’t rooted in fear or panic—it came from a place of genuine curiosity, seasoned experience, and rational analysis. He asked:

Dad’s question was simple but profound. Perhaps he was also asking, When is the next shoe going to drop?

It’s a fair question. A lot of people are asking questions like that about now. With markets at all-time highs, geopolitical tensions rising and inflation still being debated, many are nervously watching the skies for signs of storm clouds. My initial short answer to dad’s question was: The shoe will drop when it drops.

The longer answer is more interesting. Basically, while a correction is inevitable at some point, we are not there yet, and it may take some time to get there. All the available data suggest that we are in the midst of a strong bull market. And in times like these, it’s far more dangerous to jump out of the way of a bus that may be 25-miles down the road, just because you fear an accident like one read about in today’s news.

So, let’s examine the data.

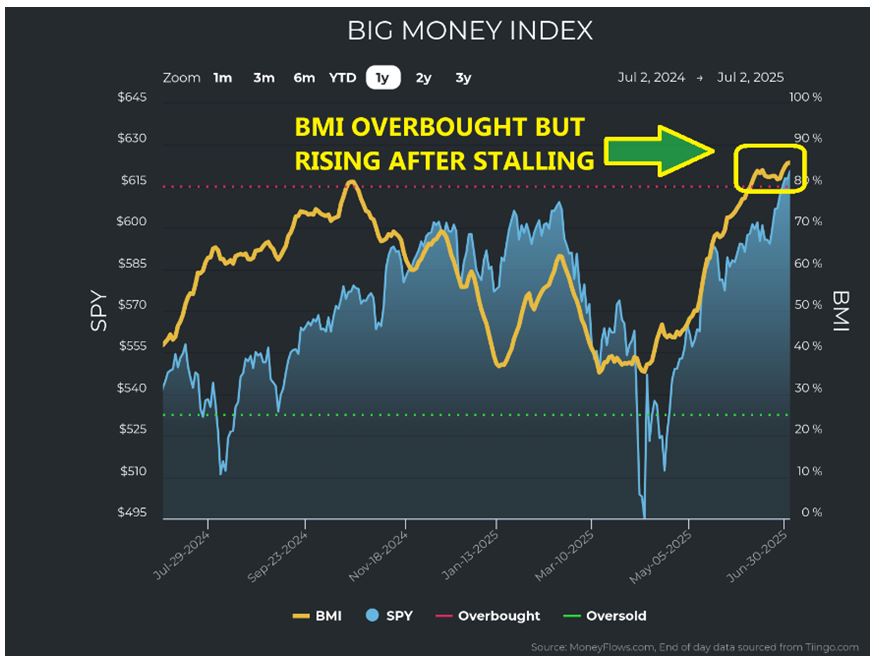

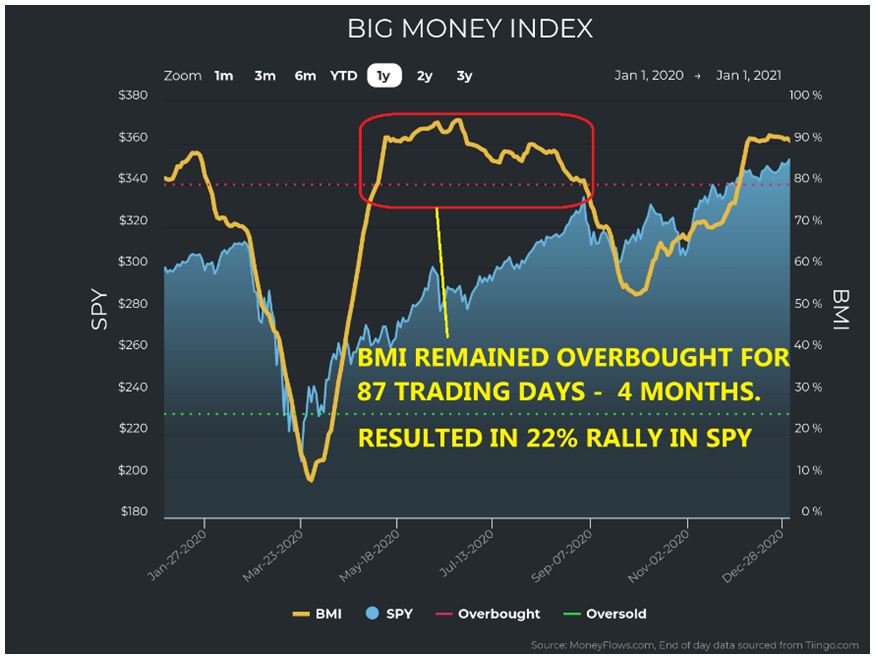

To begin with, the Big Money Index (BMI) is still sitting in overbought territory. This indicator measures large institutional buying versus selling and is often a powerful signal of the market’s direction. A rising BMI, even in overbought conditions, suggests sustained interest from big players.

Recently, the BMI drifted down slightly, but last week it began to rise again.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

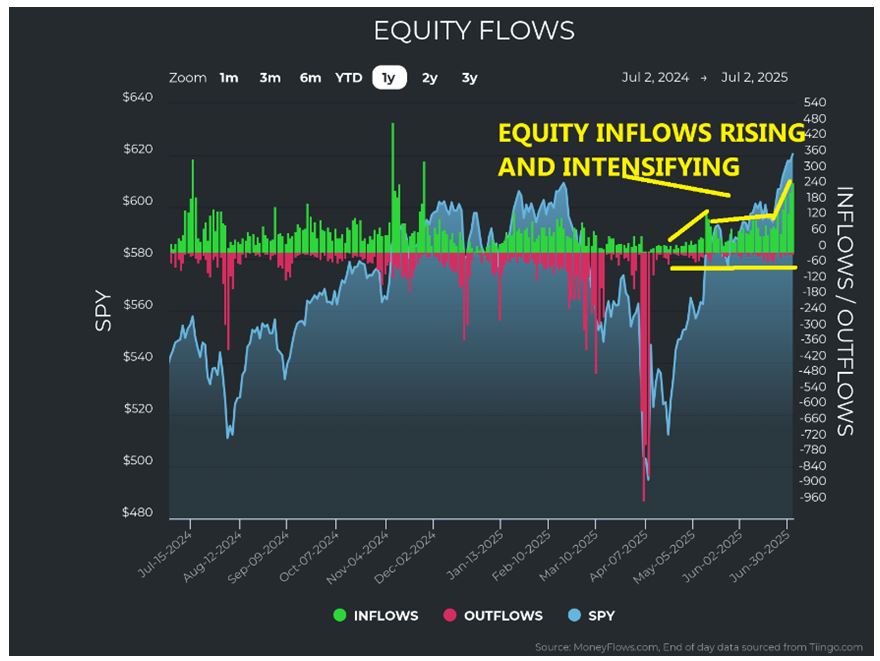

Even more telling, we are witnessing increasing equity inflows—a positive sign that institutional and retail investors alike are putting fresh capital into the market.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

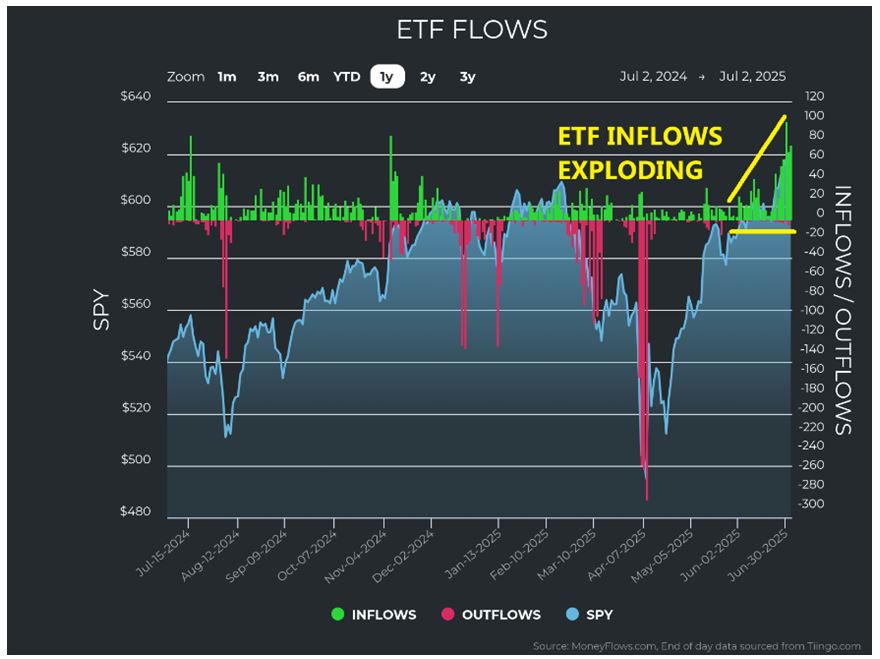

ETF inflows have exploded higher in recent weeks. This surge is significant because ETFs offer a window into broad investor sentiment across sectors, sizes, and styles. When ETF money flows accelerate, that signals growing confidence in the equity market.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

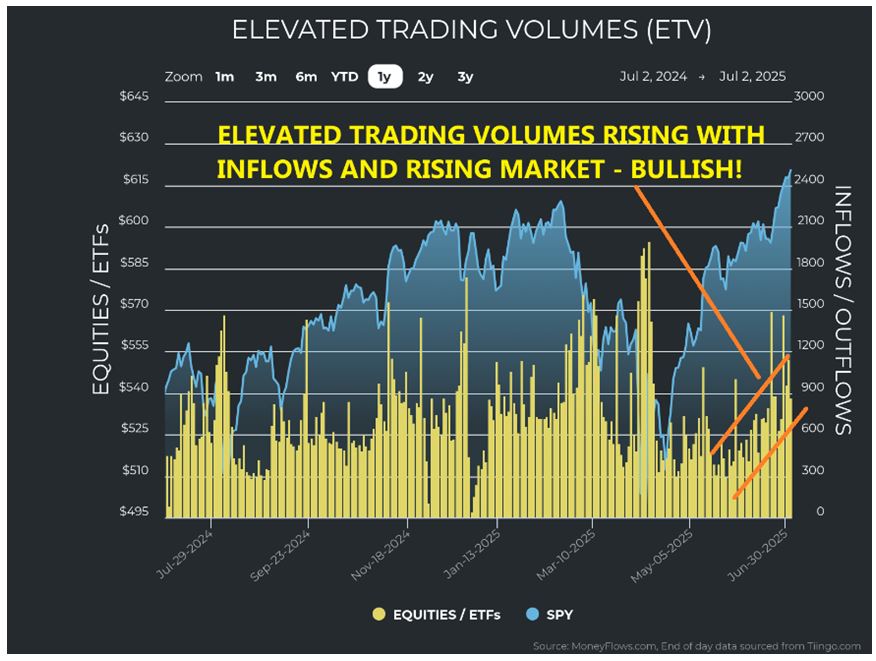

This activity has been accompanied by elevated trading volumes, which have been climbing steadily for several weeks. When volume rises in tandem with prices and inflows, it suggests conviction behind the buying. This combination often precedes a continuation of bullish trends.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Taken together, this could very well be the start—or the continuation—of a blow-off top phase. This is a point in a bull market when enthusiasm turns into euphoric momentum. In such a scenario, investors begin buying not because of rational valuation analysis, but because of Fear of Missing Out (FOMO). However, it’s important to remember that the BMI can remain overbought for an extended period. A prime example:

Following the COVID crash, the market stayed in overbought territory for a remarkable 87-trading days, about four-months. Many tried to call the top prematurely. Those who stayed invested reaped the rewards.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

A better warning trigger is when the BMI falls from overbought accompanied by clear outflow signals. That’s the real caution flag. Until then, history shows that overbought markets can keep running.

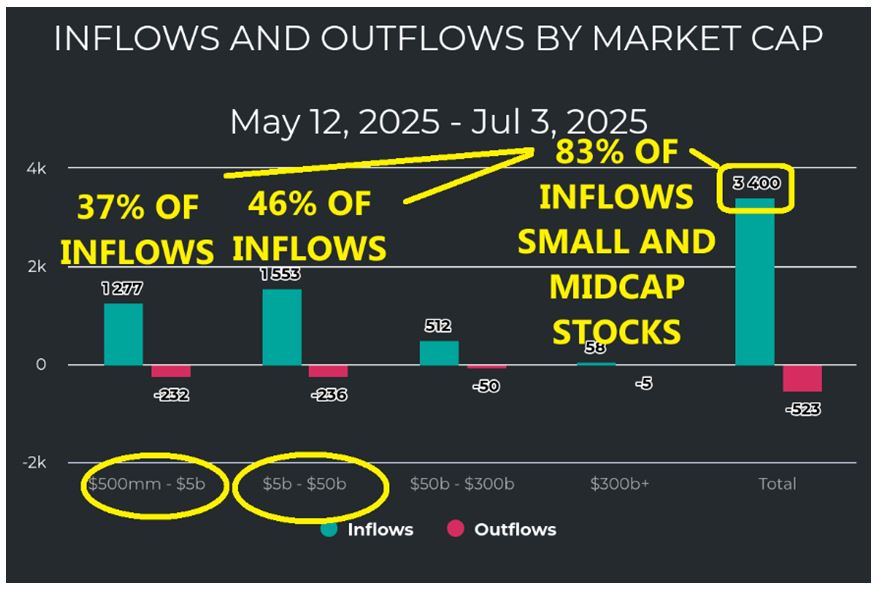

One especially bullish signal is the destination of these inflows. Capital isn’t moving randomly, as it usually targets more aggressive high-growth areas. For example, since the day President Trump announced a 90-day tariff delay, 83% of equity inflows have moved into small-cap and mid-cap stocks, which are generally more sensitive to economic optimism and future growth prospects.

When investors favor high-growth sectors, it’s often a sign that they expect strength ahead.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

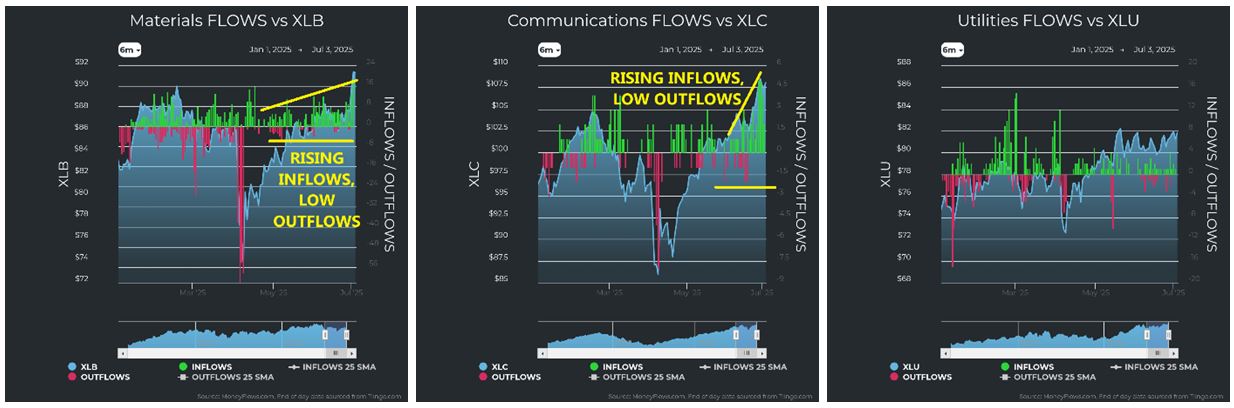

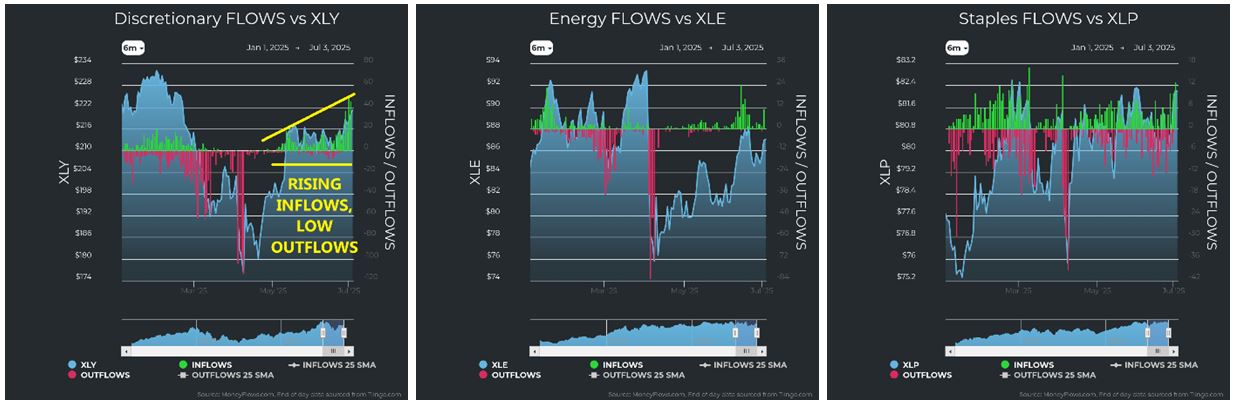

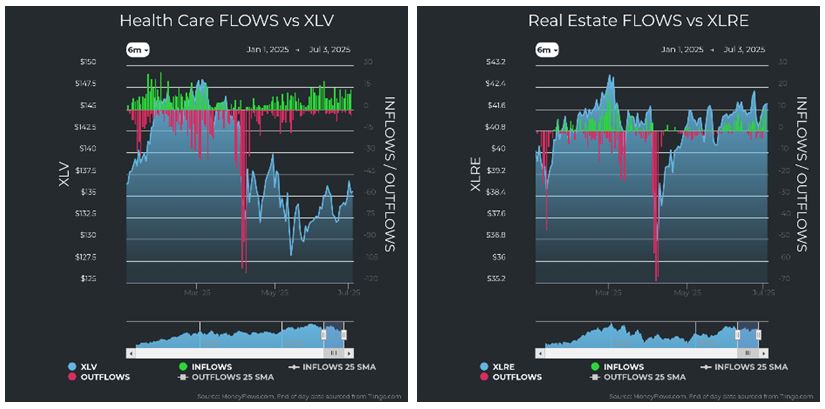

Next, we look at sector rotation. From the market lows on April 8th, we have observed a significant shift in sector leadership. Defensive sectors like Utilities, Staples, and Real Estate—which usually outperform during market stress—have dropped in rank. Real Estate also declined.

![]()

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

![]()

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

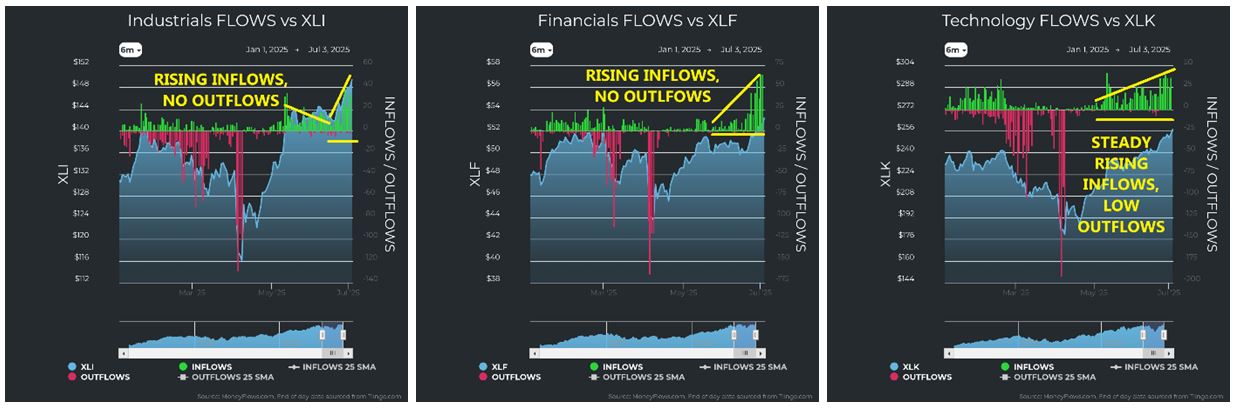

Conversely, growth sectors have surged. Technology, Industrials, and Consumer Discretionary have all seen strong upward moves in ranking. These sectors tend to thrive during periods of expansion.

If we drill down further and examine actual sector inflows, the story becomes even more encouraging. Industrials, Financials, Technology, Materials, Communications, and Discretionary stocks are attracting substantial new investment. Virtually none of these sectors are showing meaningful outflows. This tells us that the optimism is broad-based and capital is rotating into sectors closely aligned with economic growth.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

So, where does that leave us?

The market is strong. The underlying data from ETF inflows to trading volume, sector rotation to BMI strength points to continued upward momentum. That doesn’t mean there’s no risk. There always is. But there’s no evidence yet of the kind of deterioration that would suggest the proverbial shoe is about to drop.

Fear and imagination are powerful forces. They’ve misled entire societies, as history shows, with endless examples. They can just as easily mislead investors today. We must anchor ourselves in data, not in ghosts.

As Will Rogers once said, “Don’t let yesterday use up too much of today.”

Let’s take Will Rogers one step further: “Don’t let imagined tomorrows rob you of today’s opportunities.”

All content above represents the opinion of Jason Bodner of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

Which is Right? The Downbeat ADP Jobs Report or Friday’s Bullish Report?

Income Mail by Bryan Perry

Bond Equivalents Should Shine in the Second Half Of 2025

Growth Mail by Gary Alexander

Where is the U.S. Dollar Headed? – And Does it Matter?

Global Mail by Ivan Martchev

The S&P Is Flying High, Like Icarus

Sector Spotlight by Jason Bodner

How Overbought is this Market? (And Does it Matter?)

View Full Archive

Read Past Issues Here

Jason Bodner

MARKETMAIL EDITOR FOR SECTOR SPOTLIGHT

Jason Bodner writes Sector Spotlight in the weekly Marketmail publication and has authored several white papers for the company. He is also Co-Founder of Macro Analytics for Professionals which produces proprietary equity accumulation and distribution research for its clients. Previously, Mr. Bodner served as Director of European Equity Derivatives for Cantor Fitzgerald Europe in London, then moved to the role of Head of Equity Derivatives North America for the same company in New York. He also served as S.V.P. Equity Derivatives for Jefferies, LLC. He received a B.S. in business administration in 1996, with honors, from Skidmore College as a member of the Periclean Honors Society. All content of “Sector Spotlight” represents the opinion of Jason Bodner

Important Disclosures:

Jason Bodner is a co-founder and co-owner of Mapsignals. Mr. Bodner is an independent contractor who is occasionally hired by Navellier & Associates to write an article and or provide opinions for possible use in articles that appear in Navellier & Associates weekly Market Mail. Mr. Bodner is not employed or affiliated with Louis Navellier, Navellier & Associates, Inc., or any other Navellier owned entity. The opinions and statements made here are those of Mr. Bodner and not necessarily those of any other persons or entities. This is not an endorsement, or solicitation or testimonial or investment advice regarding the BMI Index or any statements or recommendations or analysis in the article or the BMI Index or Mapsignals or its products or strategies.

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities and;

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.