by Ivan Martchev

March 31, 2026

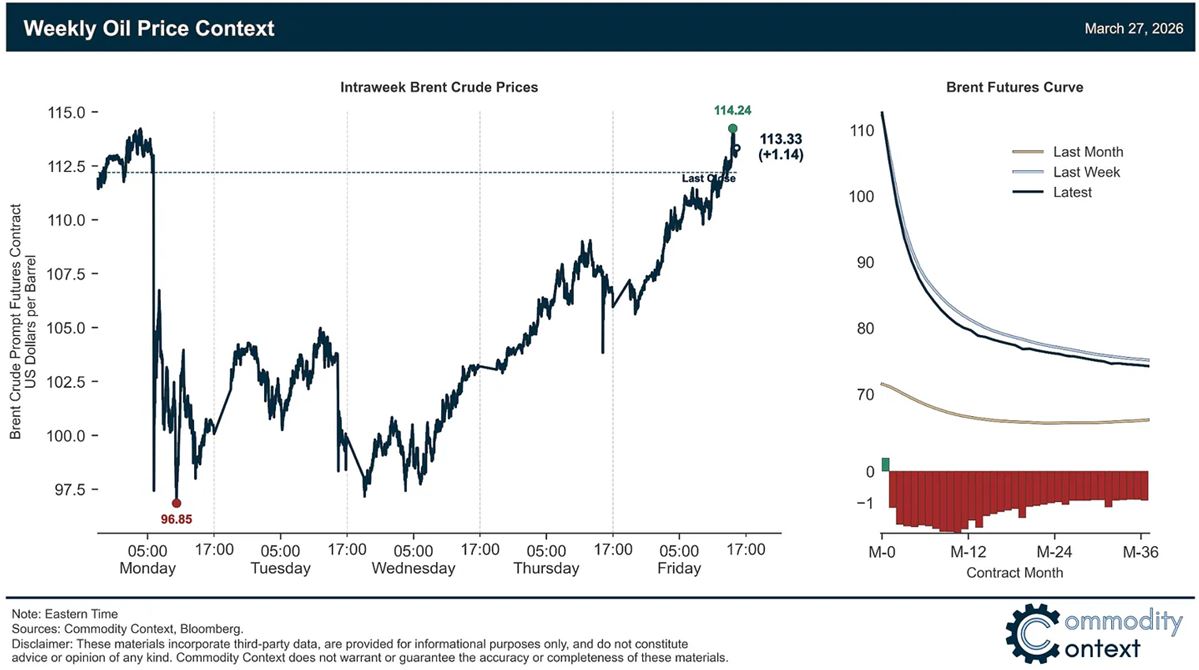

Last week’s high in S&P futures was set just about the time of the Monday morning post from President Trump, saying he was giving Iran a five-day hiatus on bombing their electricity generation plants to give diplomacy a chance. That was also the low-point of the week in Brent crude oil, at just below $97 per barrel.

Inversely, the low of the week for S&P futures and the high for Brent crude oil (above $114) was set towards the close of trading last Friday, when investors realized the President’s tweets (or “truths,” as they are labelled on Truth Social) are well…not necessarily true. This continued surge in oil came after another post on Truth Social last Thursday extending the five-day deadline for another 10-days, until April 6.

The markets ignored this more generous extension, as the Israelis kept on bombing and the Iranians kept on retaliating – despite all those presidential “truths,” and so the mess started to worsen over the weekend.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

These price swings are evident in the chart of last week’s trading in the global oil benchmark called Brent Crude. It typically trades at a premium to WTI (the U.S. benchmark). One of the key differences is Brent futures must be delivered in the U.K.’s Sullen Islands, while WTI is deliverable at Cushing Oklahoma. But crude oil actually scheduled to be delivered in Dubai are scarce, and hence much much more expensive.

Brent futures are now in “backwardation,” which means the market is in shortage, as the front-month contract is about $35-costlier than the contract a year out. The issue is the Iran war and the practical closure of the Strait of Hormuz. If the Strait is not opened and flowing within two-weeks, Brent and WTI futures will be a lot higher, as shortages that are now visible in some places globally will get a lot worse.

Let’s say the Strait of Hormuz is causing a conservative 15-million bpd (barrels per day) shortage (the actual number is closer to 20-million). Much has been said about the release of 400-million crude oil barrels from global strategic oil reserves, but few pointed out the maximum daily rate of delivery of that oil from reserves is less than two million bpd. That means the world is short about 13-million bpd with a continued Strait of Hormuz closure, even after these strategic reserves begin to flow at their maximum-rate.

If one re-routes crude oil through the Red Sea as much as possible, then the Houthis in Yemen will enter the war. The Houthis were a real menace in the Red Sea, causing container traffic to re-rout away from it. Even if unobstructed, the rate of oil traffic is tiny in the Red Sea due to the lack of pipelines to local ports.

Last week, Secretary of State Marco Rubio told G7 foreign ministers this war with Iran will last another 2-4 weeks. We also heard President Trump would meet President XI Jinping in Beijing May 14-15, after the original meeting date with XI Jinping was postponed due to the crisis situation in Iran.

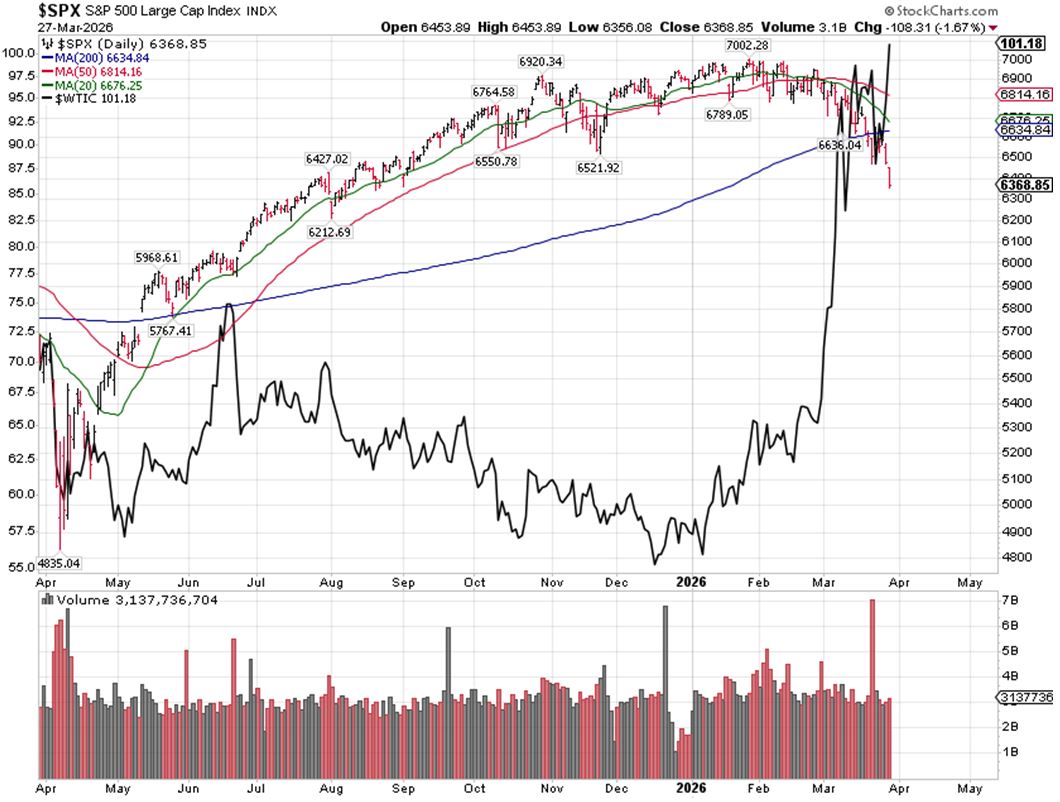

Why am I so concerned over this detailed oil discussion? Because stocks tend to fall when oil-prices rise.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

We have been locked into a trading pattern, where the higher oil goes the lower the stock market goes – ever since the beginning of the Iran war. As shortages become more visible in the next two-weeks, trading in oil futures will likely become less and less orderly, with an upside bias where the fresh all-time highs from 2008 include oil near $150 for WTI crude oil futures come into play. If the war is not over in the next two weeks, I expect to see the S&P 500 trade near either side of 6000. We closed last week at 6368.

What would successful completion of this war look like, and what would it mean to the markets?

I do not believe there will be regime change in Iran via aerial bombardment alone. Seizing Kharg Island and/or several other sites does not mean the war will be over soon. In fact, it sounds more like an escalation to me. To me, the end of the war means the bombs stop dropping on all sides, and the flow of traffic of crude oil resumes. If it takes another two weeks, then crude oil (via the WTI U.S. contract) can easily rise $20 to $30 per barrel higher from here, and it can rise further if these shortages persist.

If the war lasts another four weeks – to the end of April – as per the high end of Secretary Rubio’s comments, a fresh all-time high for WTI Cushing is highly likely. There is some damaged infrastructure already. How much more infrastructure is damaged between now and the end of the war determines how high the oil price finally settles, and that level will likely be higher than it was before the war began.

The higher the price of oil settles, the bigger the breaks in the global economy, as Europe and Asia and other places depend on LNG – despite 17-percent of Qatari LNG capacity gone for the next five-years – placing these economies at a disadvantage as their natural gas prices will settle in multiples higher than U.S. pipeline-dependent natural gas, where the front-month contract closed on Friday at $3.025/mmBTU.

April should be an eventful month. Before April is over, we could see a long-term bottom for stocks, after which I expect a sharp rally amounting to about ½ to ⅔ of the preceding decline, but at what level of the S&P 500 that rally starts will be decided entirely by when the war truly ends.