by Gary Alexander

March 3, 2026

In the first quarter of 1776, we saw three world-changing books (the first was more of a pamphlet) which changed the world, with the third-book planting the seeds that helped both Britain and America “win” the long War of Independence which encompassed 40-years of conflict, culminating in the War of 1812.

These three-books all published in the first-quarter of 1776 (actually, the first 10-weeks of 1776) were:

- “Common Sense,” by “an Englishman” (a new colonist, Thomas Paine), 47-pages, published January 10, 1776.

- “The Decline and Fall of the Roman Empire, Vol. I,” by Edward Gibbon (595-pages, February 17, 1776)

- “In Inquiry into the Wealth of Nations” by Adam Smith (over 1,000-pages in most editions), March 9, 1776.

The first book was political, the second historical, the third economic. Add in the short (single-sheet broadside) “Declaration of Independence” in July and you have two-thin slices of American political bread wrapped around generous portions of English roast beef. (This “sandwich” metaphor is particularly relevant since the “Earl of Sandwich” was the head of Britain’s Royal Navy during the Revolution).

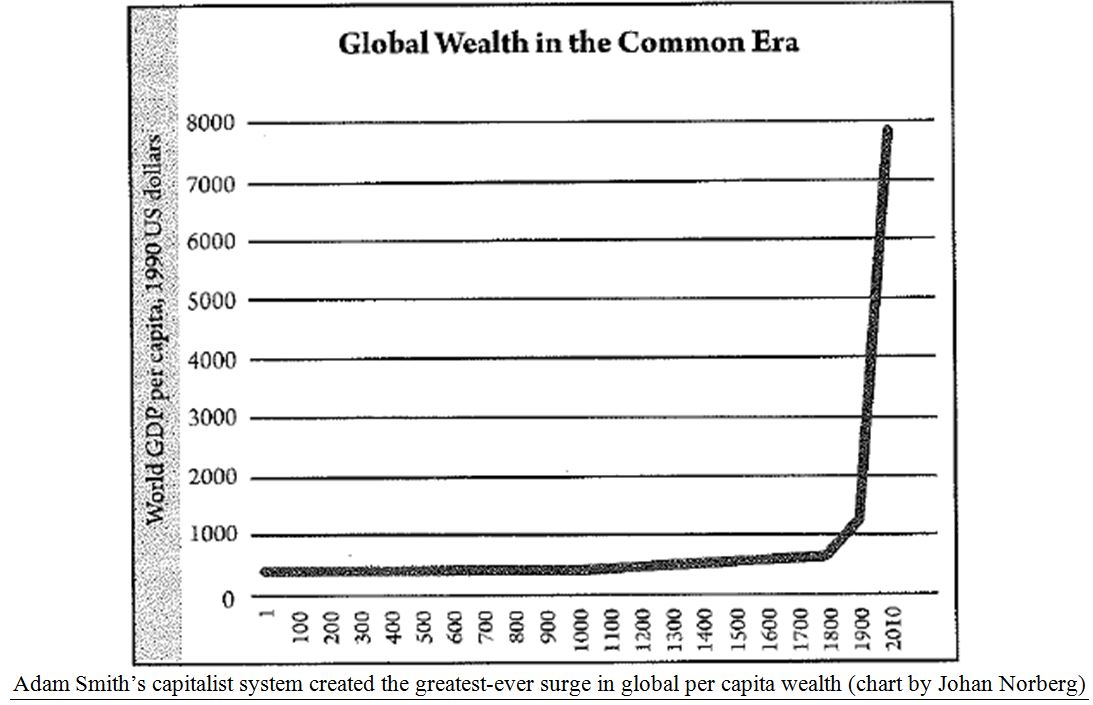

Historian H.W. Brands, in his book, “Masters of Enterprise,” says the two proclamations of U.S. political independence defined our nation’s birth while Adam Smith’s Wealth of Nations laid out the blueprint for our great success. Brands identifies a perpetual war between the political leveling mechanism of a democracy versus the excesses of our best entrepreneurs, who create new inventions and businesses to help some reach greater wealth while millions of others benefit later on from their inventions and wealth.

In other words, we often credit (or blame) our 40+ presidents and their alleged influence on the economy while ignoring or undervaluing the 40+ top inventors and business creators who made most of that growth happen. In his book, Brand profiles 25-business leaders, starting with German-born John Jacob Astor (1763-1848), first selling flutes, then furs, then real estate, and Cornelius Vanderbilt (1794-1877) – in shipping and rails – ending with technology-giants Andy Grove and Bill Gates, marketing computer hardware, chips and software, which made them filthy rich while helping most Americans enjoy a better life.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

I’m currently mid-way into the long, turgid writings of the British historian Gibbon and the Scots moral philosopher and economist Adam Smith, on the 250th anniversary of their two major works. Although each could benefit from a friendly editor – Smith spent 47-pages dissecting the history of silver’s price in England over a 500-year period – such tutorials create value when Smith summarizes the beneficial drop in prices and rise in quality in the top technology sectors of his day. In one segment (after the long silver aside), he says a watch of finer precision and craftsmanship cost 20-shillings (one-pound) then, while an inferior (and larger) watch cost 20-pounds a century ago, a 95% price drop, bringing watches to millions.

“A better movement of a watch, that about the middle of the last century could have been bought for twenty-pounds, may now perhaps be had for twenty-shillings.”

-Adam Smith, The Wealth of Nations.

Gibbons’ book is also a surprising delight. Volume I (the only volume produced in 1776) spends the first 100+ pages describing an ideal state: In the second century, Rome enjoyed 80+ years of the Antonine Caesars from 97 to 180 CE: Trajan, Hadrian, Antoninus Pius, and the Stoic philosopher Marcus Aurelius. Rome only started to go into the commode with Marcus’ successor, the aptly named Commodus.

Bear in mind: This golden age in Rome happened a century after despots like Caligula (ruling 37-41 CE) and Nero (54-68). This tells us the worst rulers may be in charge for a decade, but that does not mean the nation’s decline is imminent. There can be a healthy renaissance following such disastrous leaders.

“The prosperous state of the empire was warmly felt, and honestly confessed, by the provincials as well as Romans. They celebrate the increasing splendor of the cities, the beautiful face of the country, cultivated and adorned like an immense garden; and the long festival of peace, which was enjoyed by so many nations, forgetful of the ancient animosities, delivered from the apprehension of future danger.”

–From Gibbons’ Decline and Fall, Vol. I, Chapter II, “Internal Prosperity in the Age of the Antonines”

My compatriot here, Jason Bodner, often quotes Marcus Aurelius, the enlightened Stoic emperor. Here are some of his sample quotes, which could double as great investment advice, or simply how to succeed:

Sample Marcus Aurelius Quotes:

- On Actions: “Waste no more time arguing what a good man should be. Be one.”

- On Adversity: “The impediment to action advances action. What stands in the way becomes the way.”

- On Actions reflecting character: “If it is not right, do not do it; if it is not true, do not say it.”

- On Death: “Think of yourself as dead. You have lived your life. Now, take what’s left and live it properly.”

- On the News: “Everything we hear is an opinion, not a fact. Everything we see is a perspective, not the truth.”

- More News: “You have power over your mind — not outside events. Realize this, and you will find strength.”

Here’s a capsule of the Antonine era’s rulers…all winners until Commodus, from 95 to 195 CE (essentially the red-line represents the primary ruler, the blue-line the waiting in line for power):

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

The two-century Pax Romana ended in 180 CE – and that’s when Rome’s decline and fall properly began.

This long stretch of noble Roman rulers – centuries before Rome fell – seems to earn a better title for Volume I: “On the rise, peak and decline of the Roman Empire.” Any warning of Rome’s fall in the first-century was premature, which ties in with a famous Adam Smith quote a year after his book came out:

“There is a great deal of ruin in a nation” – Adam Smith, in a 1777 letter.

After American forces surprisingly won the Battle of Saratoga in 1777, bringing the French onto the U.S. team, a young man wrote a letter to Smith bemoaning this as a signal the British Empire would soon die.

Smith responded in a classic line, “There is a great deal of ruin in a nation,” implying it will take a lot more than some colonial rebels to bring the sceptered Isle to its knees. Sure enough, British power grew over the next century, primarily under Queen Victoria, and Britain created a rising middle-class at home.

In the same sense, a modern reading of “Common Sense” and Jefferson’s “Declaration” sound somewhat hollow in their core statements about the evils of royalty (Paine) or King George in particular (the middle listing of all the King’s faults). In a modern review of George III’s long reign show him no worse, and in some ways somewhat better, than his murderous warmongering grandfather and predecessor, George II. King George wasn’t “made,” at least not in the war-years. As for Thomas Paine’s screed against royalty, it’s humbling (to those wishing all kings dead) to see America rely on troops authorized by the kings of France, Spain and other European monarchies to squirm out of their underdog position in the late 1770s.

Some More Recommended Books

While I certainly recommend reading Adam Smith, Thomas Paine and Edward Gibbon in the original, I have consulted well over a dozen books for this article, including six-wonderful economic history books by H.W. Brands, six by U.S. Revolutionary era historian Gordon Wood, a Revolutionary novel series by Jeff Shaara, two-masterful war sagas by Rick Atkinson and a fine 1776 survey by David McCullough.

I have not yet begun assembling my top 10-books for 2026, but I don’t think Jeremy Grantham’s “Making of a Perma-Bear” published January 13, will make the list. He consistently underrates our resilience. I’m reading a better book now, published last week, John O. McGinnis, on “Why Democracy Needs the Rich.” There are several reasons to honor the rich, as Adam Smith says innovative products cost a lot of money to build prototypes. Only the rich customers can afford to buy these products and return the cost of development, but eventually all of us benefit. We see that in every technological advance in U.S. history.

This new McGinnis book offers détente between the 1776 warring documents: Democracy vs. Wealth – the Common Sense-Declaration political path versus Adam Smith’s road toward greater overall wealth.

I’d love to recommend 15 or 20 more books here, but to choose only three, I’d start here:

Rick Atkinson’s latest Revolutionary War opus, “Fate of the Day” deserves a spot on this list since it superbly dramatizes the fact that America had no business, literally no chance, of winning freedom in the years 1777-79, but a series of seeming miracles made it come out right for us later, in Yorktown harbor.

Happy reading, Happy 250th Birthday to America and – more importantly – to our 1776 founding ideals.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

The U.S. Remains the World’s Primary Economic Oasis

Income Mail by Bryan Perry

High Yield Investments Benefit from This Market Reset

Growth Mail by Gary Alexander

The Seeds of Growth Were Planted 250-Years Ago…

Global Mail by Ivan Martchev

The Iran War Begins, But Where Will It End?

Sector Spotlight by Jason Bodner

A Long-Term Perspective Makes Investing Success Likelier

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20-years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.