by Ivan Martchev

March 24, 2026

According to mainstream dictionaries (via Google’s Gemini), “Force Majeure” is a contractual clause freeing parties from liability when extraordinary, unforeseeable events—like natural disasters, war, or pandemics—make performance impossible or impractical. Based on the French legal term for superior force, it requires strict, timely notice and direct causation to suspend or terminate obligations.

An Iranian missile hit on Qatar’s largest LNG plant seems like “direct causation” to me, and it came as a retaliatory strike for an Israeli hit on Iran’s largest natural gas field, which Iran shares with Qatar.

It seems to me Israel is probing to see if the Iranians have missiles left to retaliate. (Note to Israel: Stop this probing, as one more try could put Europe in a recession.) Europeans thought they could wean their economies from cheap Russian natural gas and switch to LNG, where Qatar is a key player. Whoever blew up Russian pipelines to Europe surely was not calculating Qatar’s LNG output would shrink by 17% in the next five-years (current estimate) from one Iranian missile-hit, and the war is not over.

LNG is great if there are no pipeline options. If there are, it is not competitive, as it can be multiple times more expensive – as it has to be liquefied, shipped via a custom built tanker, and liquefied to run over local networks, making it uncompetitive to pipeline options, if they exist. Not only is the Strait of Hormuz not fully operational, but insurance is so high that, even if there are no issues with Iran, it makes energy too expensive, but even if the Strait is open, 17% of Qatar’s output is gone for the foreseeable future.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Last week’s front-month Rotterdam natural gas futures got as high as 74 EUR/megawatt hour, which for U.S. price comparison is like $25/mmBTU (our front month gas is a little over $3). During the Ukrainian war, those same Rotterdam futures got into the EUR 340s, but let’s not see that again, as the economic consequences for Europe would be gargantuan. Under a force majeure scenario, companies thinking they had natural gas supply for up to five years may no longer have it, as part of the capacity no longer exists.

It would appear the Trump administration is preparing the Marines to land on Iranian soil, just in case other methods are not working (hint: they are not). The most obvious target for Marine boots on the ground is Kharg Island (see map, above), which handles the majority of Iranian oil exports.

Other U.S. administrations have mulled seizing export sites in order to use them as bargaining chips against Iran in prior conflicts. Be that as it may, any landing of U.S. forces on Iranian soil does not suggest a de-escalation, as it suggests a much longer conflict than most investors fear right now.

Right now, the situation resembles a tit-for-tat escalation. Israel seems to be trying out the Iranians by hitting oil, natural gas and civilian infrastructure, and every time the Iranians have retaliated by lashing out at easy targets in Qatar, UAE and other close in-range places. Israelis went a step further by attacking an Iranian nuclear power plant and the Iranians hit a building inside an Israeli nuclear facility.

Given that every attempt to see if the Iranians would respond in kind has come out positive – meaning they have responded – it is a bad idea to hit Iranian electricity generation plants as an ultimatum to reopen the Strait of Hormuz, as I can see bad things happening to civilian infrastructure in the Gulf.

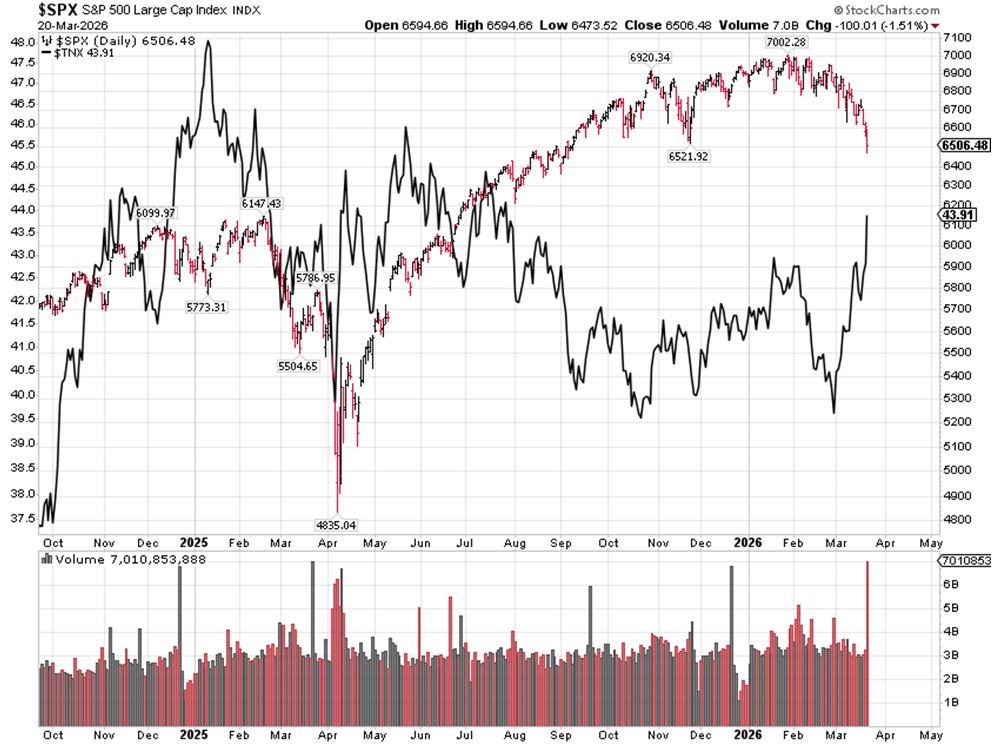

I’m presenting this war discussion in some detail because it pertains to the U.S. stock and bond markets, which are under pressure and accelerating to the downside. Long-term interest rates are rising while stock prices are falling. (We marginally traded below the November 2025 low on Friday).

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

The situation we now face is very simple: If investors see escalation and no end in sight for the war, they are likely to keep selling, and the economic consequences get bigger and bigger each day it continues. If investors were to see deescalation and a clear path towards the end of hostilities, the stock market will rally dramatically, possibly making new highs as the worst case scenarios are quickly being priced out.

As thing stood on Sunday, I don’t see any signs of de-escalation, but I sure hope I see them this week.