by Gary Alexander

March 17, 2026

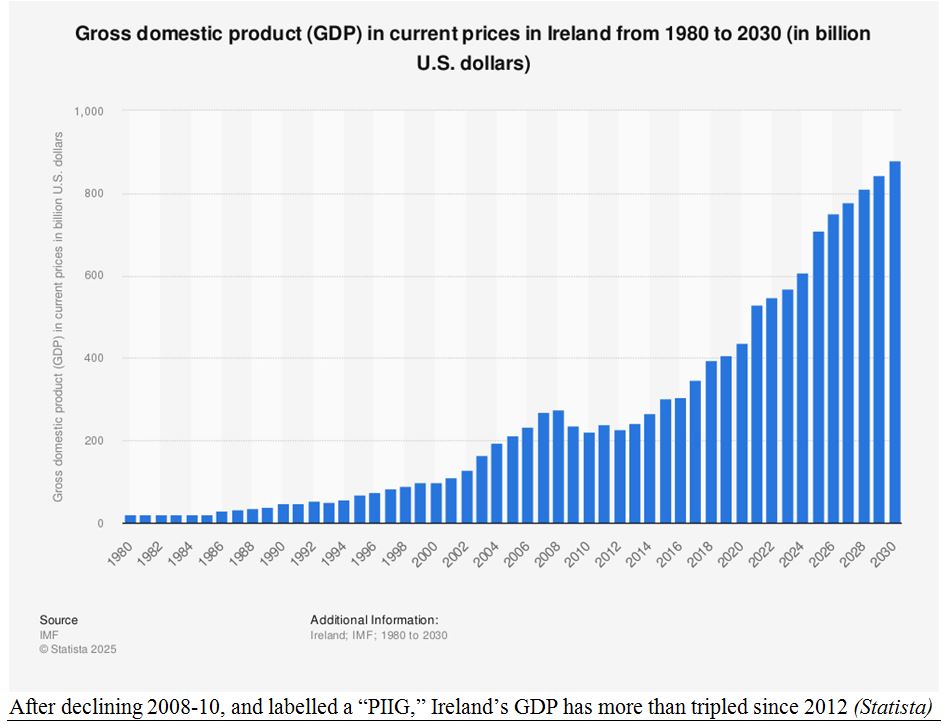

In 2025, Ireland won the gold medal for growth in Europe, as its GDP soared 10.7% for the full year, with low inflation (under 2%), and record high employment, showcasing Ireland’s remarkable comeback from being one of the five ailing “PIIGS” (Portugal, Italy, Ireland, Greece and Spain) a dozen years-ago.

Ireland’s GDP has risen (in current U.S. dollar terms) from $200-billion in 2010 to $700-billion last year:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

What is the secret of Ireland’s rapid resurrection within an otherwise slow-growth European Union?

Ireland’s foremost engine of growth has been its ultra-low corporate taxation rates, set at 12.5% in 2003. Those rates were cut in half to 6.5% for Knowledge Development companies doing R&D in Ireland. This fact caused great gnashing of teeth at Janet Yellen’s Fed, when she pushed for a “minimum global corporate tax rate” of at least 15%. In 2024, Ireland finally relented and raised its corporate rate to 15%.

Ireland has also aggressively pursued foreign direct investment (FDI) by the U.S. and other major global powerhouses. They have so far lured over 1,000 multi-national corporations to invest in Ireland, including most of the Mag-7 giants. One impact is foreign-owned companies now comprise 93% of Irish exports.

Obviously, capital migrates to nations where it is most welcome, and Ireland is the most welcome nation for capital investment in Europe. As a result, Ireland’s 2025 growth rate was six-times the EU as a whole and double any other nation in Europe: The silver and bronze medals go to micro-nations Monaco (+5.4% GDP) and Moldova (+5.1%). Meanwhile, the three biggest EU powers were very close to a recession, including Germany (+0.3%), Italy (+0.6%) and France (+1.0%), with the Finnish economy below zero.

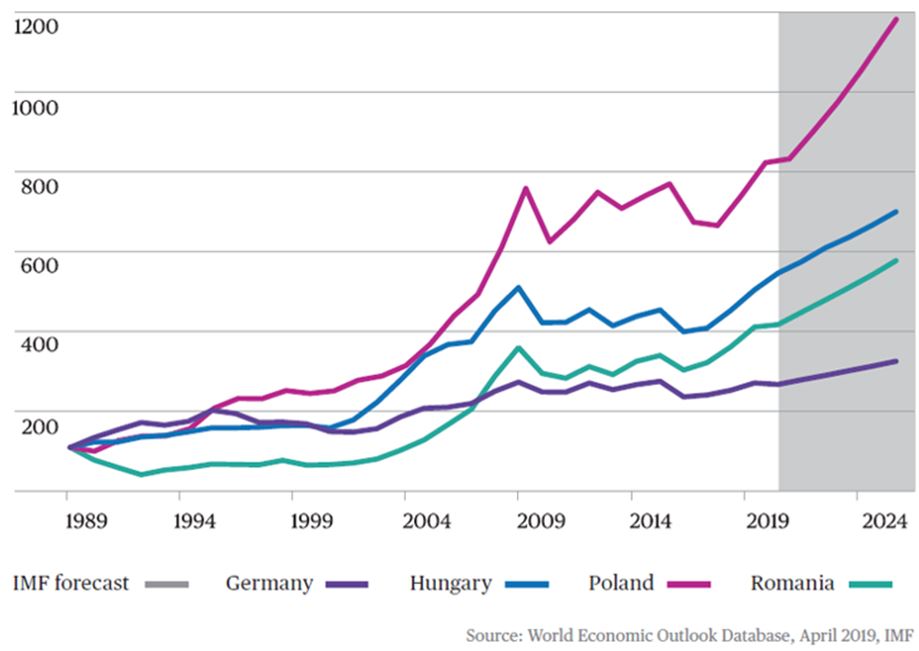

Silver and Bronze Medals Go to Eastern Europe – With Poland as the Other Rising Star

In Eastern Europe, Poland is the best economy, at +4% growth, and Poland boasts the best growth of any mainland European EU economy since 1990, due in large part to its free-market economic policies.

Since the fall of the Berlin Wall, Poland has far exceeded any other EU economy, with two other former Communist Soviet satellite nations (Hungary and Romania) eclipsing German growth (chart, below).

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Ireland and Poland show the rest of Europe how low-taxes and hard work can reap big rewards, while the other, more sclerotic, European giants (Germany, France, Italy and Spain) are chronically slow-growth economies, with massive unfunded welfare benefits, restrictive labor regulations and ultra-high tax rates.

It’s important to remember peace in Ireland and Poland must also be credited, starting with Poland’s spectacular growth spurt starting at the end of the Cold War in 1990, while Ireland’s key to future growth began with the end of a 30-year nightmare of “Irish Troubles,” ending with the “Good Friday Agreement” (the Belfast Agreement) in 1998. The end of these conflicts delivered a Peace Dividend to Ireland and Eastern Europe.

Something else, even more dramatic, happened in Ireland two-centuries ago, benefitting America greatly.

The British-Fueled Irish Famine Created Millions of Irish Americans

In re-reading Adam Smith’s massive “Wealth of Nations” this month – on the 250th anniversary of its publication – I noticed Smith taking a long, late “Digression concerning the corn trade and corn laws.”

Smith was referring to the Corn Law of 1773, but these Corn Laws were greatly enhanced and enforced from 1815 to 1846. (The term “corn” refers mostly to banned cereal grains, like wheat, oats and barley, not corn). These laws were mostly a way for Britain to “starve Ireland into submission” 200+ years ago.

High British tariffs on grains kept those grain prices too high for impoverished Irish farmers. In addition, Britain also required massive amounts of wool to feed its textile mills, so the Irish were forced to graze sheep instead of grow grains and came to rely on potatoes for the bulk of their diet. During the potato famine of 1845 to 1852, perhaps a million Irish died and another million made their way in “coffin ships” (similar to slave-ships) to the U.S., even though the Corn Laws were eventually repealed in 1846.

H.W. Brands wrote, in “American Colossus” (2010), chapter 9: “Of those Irish who didn’t die, some million and a half made their way to America [where] Irish laborers built the Union Pacific and other railroads; Irish miners dug coal from the hills of Pennsylvania,” but most remained in Eastern cities: “On the eve of the Civil War more than 80-percent of unskilled labor was Irish. Their employers appreciated their willingness to work for low wages – even as many of those employers despised the Irish as barely human.” Brands added: “The Irish were loved even less by the workers they displaced, in particular African Americans.” Frederick Douglas said, “Every hour sees us elbowed out of some employment to make room for some newly arrived emigrant from the emerald isle, whose hunger and color entitle him.”

Unable to buy their way out of the Civil War draft (for $300), roughly 200,000-Irishmen served in the Union Army, about 20% of them killed in action. Then, they went back to their “dirty work” jobs. By 1870, says Brands, “the Irish composed more than a fifth of the populations of New York and Boston,” enough to “swing elections in New York City, and State, in Boston and Massachusetts and, in tight races, in the nation as a whole.” In fact, some notable heirs of Irish immigrants became our presidents: John F. Kennedy was a great-grandson of potato famine refugees, and Ronald Reagan was son of an Irish father.

Automobile magnate Henry Ford was the son of a Cork immigrant; dramatist Eugene O’Neill was son of a Kilkenny immigrant; and dancer Gene Kelly was grandson of a refugee sailing out of Derry, Ireland.

This is another example of how immigrants helped built this nation, often after being forced out of their land of origin. To this day, millions of refugees are still trying to enter the U.S. to work low-wage jobs.

Let me close with a toast to the Irish – to those now living in America and those in the Emerald Isle.

The real Saint Patrick was born around 389 CE, with March 17 being his presumed death date in 461, not his birthdate. Some other famous Patricks born March 17 (or 16) include two “Model Major Generals”:

- Patrick Connor, Union Major General, born in County Kerry, Ireland on March 17, 1820.

- Patrick Cleburne, Confederate Major General, born in County Cork, Ireland, March 16, 1828.

- Patrick Duffy, actor in the “Dallas” TV series, was born March 17, 1949.

- Daniel Patrick Moynihan, the Irish American U.S. Senator, was born March 16, 1927, and

- An Irish Lass, the First Lady Pat (Ryan) Nixon, was born March 16, 1912.

Happy Saint Patrick’s Day!

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

Will Oil Prices Reach the Stratosphere – or Retreat Soon (or Both)?

Income Mail by Bryan Perry

A New Golden Buying Opportunity?

Growth Mail by Gary Alexander

Ireland is Europe’s Strongest Economy – Happy Saint Patrick’s Day!

Global Mail by Ivan Martchev

The Longer the War, the Worse the Economic Impact

Sector Spotlight by Jason Bodner

Where There’s Market Smoke, There’s Fire – But Where’s the Fire?

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20-years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.