by Gary Alexander

March 10, 2026

Hardly a week goes by without a new warning that AI will costs millions of jobs – heck, maybe even 300-million jobs by 2030. One early report (2018) predicted a loss of up to 800-million global jobs by 2030.

A more modest 2023 report forecast AI could impact 300-million jobs, and more recently, Anthropic CEO Dario Amodei predicted AI could wipe out half of all entry-level jobs from 2025 to 2030. Also, the latest World Economic Forum estimated 92-million jobs would be displaced by 2030, although they were sane enough to counter this with 170-million new jobs being created, but firings, not hiring make headlines.

Last week’s Wall Street Journal covered a new Goldman Sachs report saying AI will eventually displace 11-million jobs – above 6% of U.S. workers. The report also talked about a corresponding 30% gain in productivity, boosting GDP and corporate earnings, but the loss of 6% of workers earned the headline, since bad news sells. The report also said companies that discussed AI in the fourth-quarter “cut their job openings by 12%,” but any list of job openings implies new hires, more jobs ahead, replacing posts lost. (“Goldman Sachs Predicts AI Will Eventually Displace 6% of U.S. Workers,” Heather Gillers, WSJ, March 3, 2026).

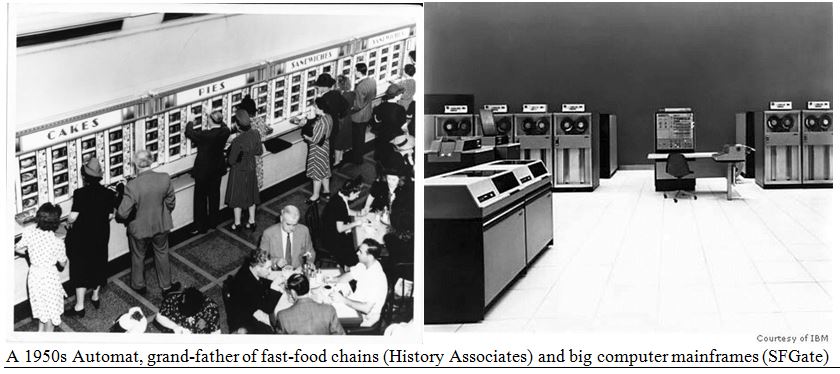

I’ve heard these scary stories several times in my 80-years. When my father took me to New York City 70-years ago, he showed me some new modes of transportation and dining, including waiter-free dining in a huge room called the Automat, run by Horn & Hardart. You put in a few nickels or dimes and opened the vault to a delicious slice of blackberry pie, my weakness. Dad and several others said this new technology would put restaurants out of business, but instead this style of impersonal dining led to the birth of fast food chains, which didn’t exist until those Golden Arches began spreading across the nation in the 1960s.

In 1968 and in the late 1970s, I worked in a computer-center where giant Big Blue mainframes were predicted to put millions of clerks and book-keepers out of work. Instead, these big computers gave birth to a new generation of smaller business and personal-computers which employed millions in new fields.

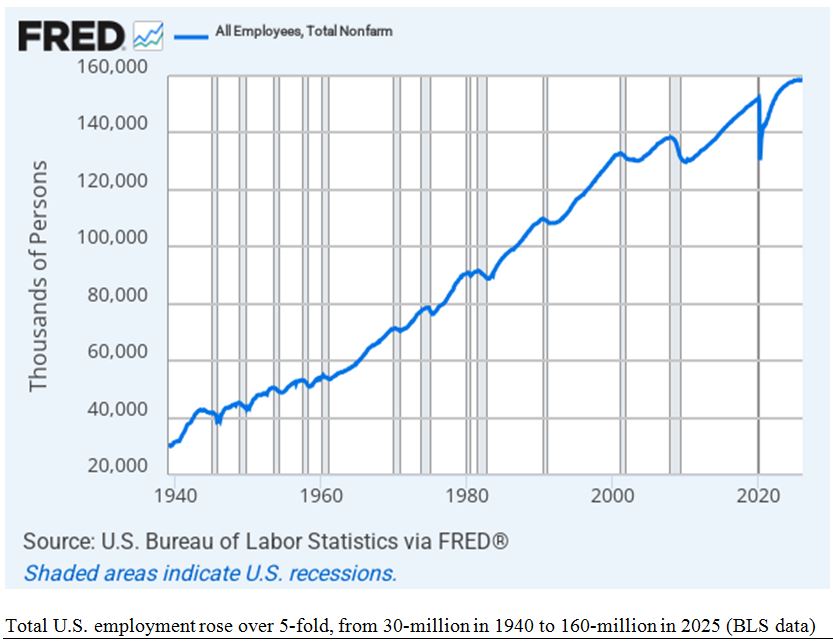

Long-term, as the following chart shows, America has created an average of 1.5-million net new jobs per year since 1940, as our robust economy easily absorbed massive new waves of workers: Baby boomers (born 1946 to 1964), former housewives entering the labor force, and millions of new immigrants:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

This trend began long before 1940. John D. Rockefeller’s low-cost kerosene put whale hunters in dry-dock. Autos and trains put horseshoe makers and carriage makers out of work. Telephones put telegram clickers on hold. Companies are always at risk if they don’t keep up with newer and better technologies.

Back in the 1930s, John Maynard Keynes, the dominant economist of that decade, warned of a coming era of “technological unemployment.” Others called industrial automation a “Frankenstein monster” destined to destroy jobs and a committee of dominant Keynesian economists of the 1960s warned President Lyndon Johnson about a “cyber-nation revolution” (computers) wiping out manual labor.

Last Friday’s Jobs Report Deepened the Job Market Gloom

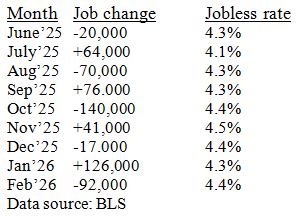

Last Friday, the market continued its gloomy late-winter mood after the February jobs report came out, saying we’ve seen a job loss of 32,000 since June, while the jobless rate rose from 4.1% in July to 4.4%:

One thing to notice in this list is the alternating rising months (July, September, November and January) with answering negative months. There’s no consistency in this data, although it says we’re losing jobs.

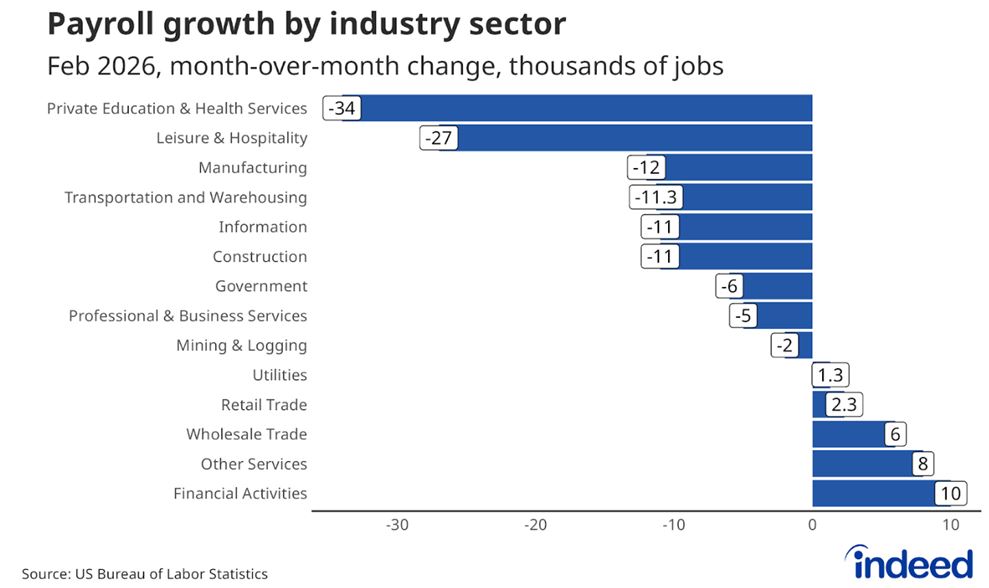

Turning to the kinds of jobs lost, the information sector only lost 11,000-jobs in February, far exceeded by health services (-28k), due mostly to labor union actions, and leisure and hospitality (-27k), so the loss of jobs by computer programmers to “AI” bots needs some rethinking (as jobs are needed to monitor AI).

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

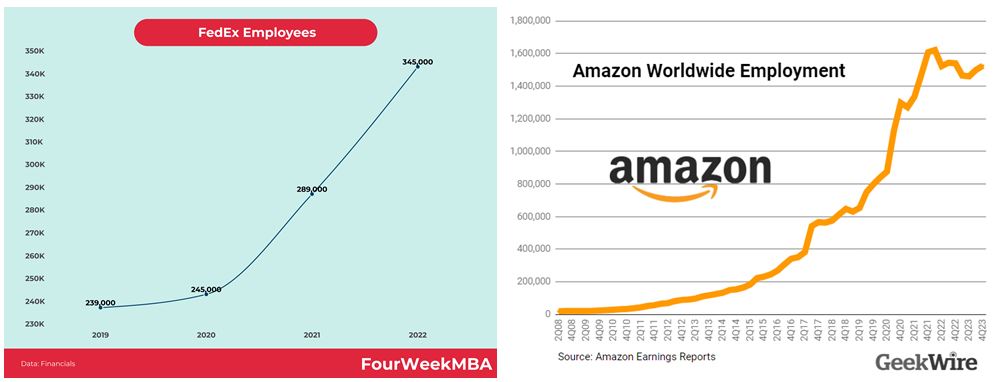

Almost daily we read of companies laying off 4,000 or 10,000 or more, but mention is seldom made of the millions of new-jobs these companies created during the previous decade. For instance, the big headlines declared 4,000-layoffs at Fed Ex, but do you recall any headlines covering their 100,000 net new-hires from 2020 to 2022? In a more extreme case, we’ve been assaulted by news that Amazon has eliminated approximately 30,000 “corporate roles” in 2025 and early 2026, but do you recall any headline covering the 1.4-million new jobs Amazon created, 2015 to 2022? (Hiring seldom make the headlines).

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Based on history, I’ll predict AI may reduce demand for certain jobs, but it will inevitably create more positions than it eliminates, as savvy workers and companies will adapt to these emerging technologies.

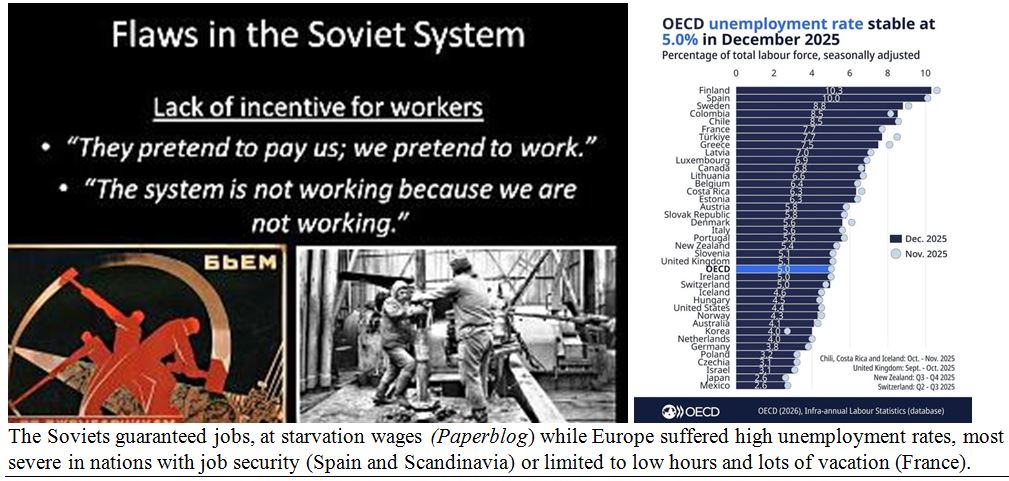

Jobs are never guaranteed – except for tenured college professors, I suppose – but this sort of dynamic job market is also a recipe for national growth. Any guaranteed lifetime employment leads to what Soviet workers mumbled: “They pretend to pay us, so we pretend to work.” Nothing creates an economic crisis more than “guaranteed employment,” (translation: few are hired). Europe’s unemployment rates were in double-digits from 2001 to 2015, but the EU has recently learned how to rethink their “guaranteed jobs.”

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

After spending 64-years in the U.S. Labor Force – starting in 1962 at age 16 with a 22-mile paper route covering a major new Seattle suburb, I moved on to being a night janitor in college, then mail-answering editor, news bureau researcher and then financial journalism by age 22. I’ve had to change the nature and location of my work several times since 1962. Smart workers will always look for greater job security by being irreplaceable in the talents they offer, showing willingness to learn and serving the customer well.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

Friday’s Downbeat Jobs Report May be Misleading

Income Mail by Bryan Perry

Three Compelling High Yield Opportunities

Growth Mail by Gary Alexander

Will AI Really Destroy America’s Job Market?

Global Mail by Ivan Martchev

When Oil Reverses, the Stock Market Will Bottom

Sector Spotlight by Jason Bodner

Don’t Let Market Volatility Upset You

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20-years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.