by Gary Alexander

December 30, 2025

Last week’s revision in GDP statistics revealed a surprisingly robust 4.3% annualized growth rate in the third-quarter, following +3.8% in the second quarter, averaging 4% growth since April 1st. After this GDP report was released, The Wall Street Journal said: “Robust spending by U.S. consumers drove greater-than-expected economic expansion in the third-quarter, and the strongest growth rate in two-years.” At the same time, the Atlanta Fed’s opening GDPNow estimate for fourth-quarter growth is +3%. (They would have submitted several previous estimates, but the hiatus in federal statistics interrupted their forecasts).

Perhaps we can now crow a bit for Louis Navellier’s year-ago prediction of 4% growth in 2025 and 5% in 2026, in our Market Mail for December 24, 2024. Here’s the headline and first paragraph of that report:

“U.S. GDP Will Hit 4% in 2025 – and 5% in 2026, if We Can Grow on All Cylinders”

“The U.S. is one of the few counties in the world that can keep growing due to better demographics. Most of the world is experiencing a population decline, except for Brazil, India and the U.S. We still have some pro-family regions – like the South and Mountain West – so our household formation continues to grow. Furthermore, immigrants are more quickly assimilated in the U.S. than in Europe. This also boosts more household formation. Also, our 50-states are very competitive with one another. They are effectively economic laboratories that can stimulate economic growth as some of the lower-tax business-friendly states – like Florida, South Carolina, South Dakota, Tennessee and Texas – have demonstrated. As a result, 5% GDP growth is possible in the U.S. – if we can grow on ‘all cylinders’ by 2026.”

–From Louis Navellier’s Market Mail of December 24, 2024.

At the time, this prediction seemed outlandish to most pundits – especially after the “Trump Tariff Tantrum” last April – but by the end of 2025, Louie’s prediction has gained some favorable press coverage, now that we’ve reached 4% growth and seem on the verge of reaching 5% GDP growth.

It’s astounding (to me) that most of the press reports over the GDP data last week said that this robust growth rate came as a “big surprise” to most economists, but not to us – or to Kevin Hassett, President Trump’s chairman of the Council of Economic Advisors (CEA). And now, tax cuts from the mid-year spending bill will take effect on January 1, 2026, putting more money in Americans’ pockets.

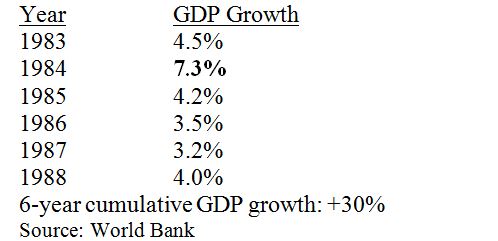

Massive tax cuts generally deliver outsized growth, as happened after the early 1980s Reagan tax cuts:

This growth spurt tells us: (1) There was never a hint of recession in 1987, and no fundamental cause for the 1987 market crash. (2) A spectacular boom year (like 1984) often begets an election landslide, as happened with Reagan’s 49-state re-election in 1984. And now, if GDP soars in 2026, the Republicans could maintain their control in Congress after next November’s mid-term elections. And (3) This six-year growth spurt in the 1980s did not revive inflation – and inflation should also stay tame throughout 2026.

Now, let’s turn to the source of U.S. economic growth in five great publications from 250-years ago:

The Top 5 Books of 1776 – A Miracle Year in America’s Birth Year

This week, America enters its “semi-quincentennial year.” That’s the clumsy term for a 250th birthday. It literally means “half of 500-years,” a needlessly complex formula. I prefer a “quarter millennium,” but “America at 250” is even better – more easily deciphered than these academic algebraic descriptors.

I’ve just finished a two-part series on the top 10-books of 2025, but nothing will ever top the impact of the top-five books of 1776 – 250-years ago this coming year – so let me start by flying a new year’s flag.

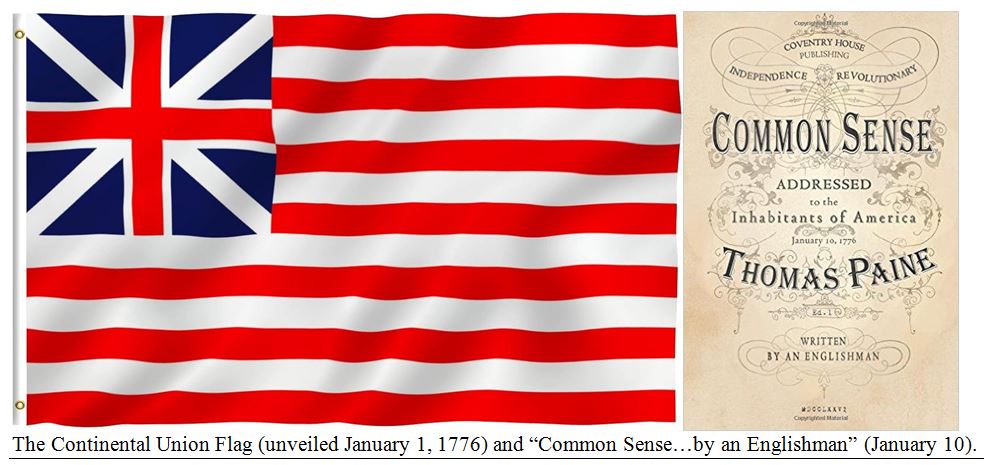

On New Year’s Day 1776, General George Washington – before pulling out of Boston for New York – ordered a new Continental Union flag raised atop Prospect Hill, overlooking Boston harbor. Like the current flag, it featured 13-red and white stripes, but it also had a British ‘look’ in the upper left corner.

At the start of 1776, the American Revolution seemed inevitable, as “rebels commanded each of the 13-colonies. Several royal governors had fled to ships offshore. But People within the colonies remained divided” (from Geoffrey C. Ward and Ken Burns’s book on “The American Revolution,” page 147).

Then, on January 10, Thomas Paine, an Englishman who had just landed in America 14-months prior (in November of 1774) wrote a 47-page pamphlet called “Common Sense,” which became the all-time best-seller in U.S. history, when adjusted for population. With a colonial population of just 2.5-million, over one-million (at least one per household) bought this incendiary pamphlet, which tipped the balance from one-third Loyalist, one-third colonial rebels and one-third neutral – to about 60-30-10 for independence.

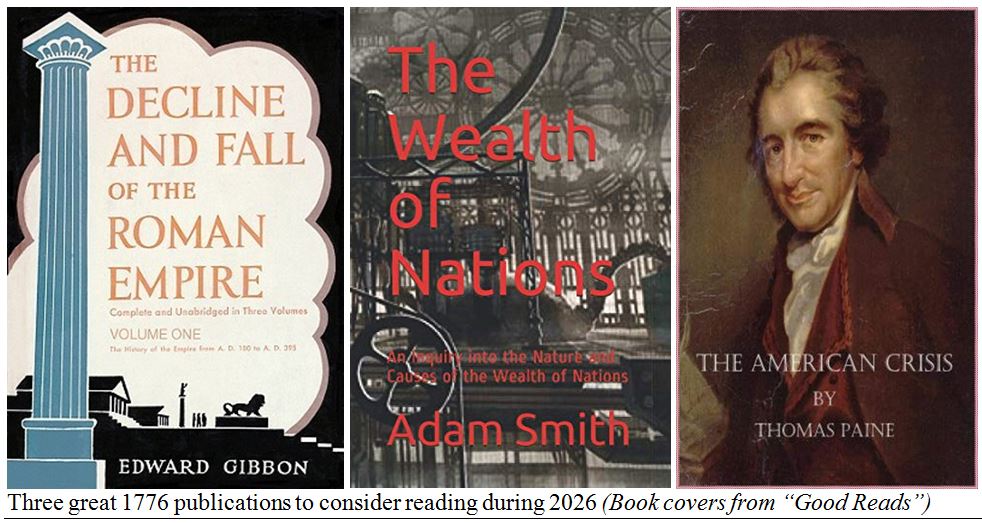

Paine’s epochal call to arms was quickly followed by major studies published in Great Britain – Edward Gibbons’ first (of six) volumes of “The Decline and Fall of the Roman Empire,” a not-so-hidden analogue to the reigning British Empire. Gibbons’ prose seemed to echo the core of Paine’s anti-Royalist views, but emerging from England’s shores. First, Paine wrote, “Hereditary succession is an imposition on posterity…giving mankind an ass for a lion,” then Gibbons echoed: “Of the various forms of government which have prevailed in the world, hereditary monarchy seems to present the fairest scope for ridicule.”

Here are the publication dates for these five earth-shaking publications of 1776:

- January 10: Thomas Paine’s “Common Sense (authored “by an Englishman” in America).

- February 17: Edward Gibbons’ “Decline and Fall,” Volume 1 (of 6), published in England.

- March 9: Scotsman Adam Smith’s economics opus, “An Inquiry into the Wealth of Nations”

- June 28 (date presented to Congress): Thomas Jefferson’s “Declaration of Independence.”

- December 19: Thomas Paine’s “American Crisis,” on “The times that try men’s souls.”

Most of us educated before the “woke police” took over know the timeless preamble to the Declaration, and Paine’s “American Crisis,” but a brief quote from each ought to impress and inspire us once again:

“We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Happiness.”

– From “The Declaration of Independence,” published July 4, 1776.

Walter Isaacson, a superb biographer, recently wrote a book calling this “The Greatest Sentence Ever Written.”

“These are the times that try men’s souls. The summer soldier and the sunshine patriot will, in this crisis, shrink from the service of their country; but he that stands by in now deserve the love and thanks of man and woman.”

– From “The American Crisis,” published December 19, 1776.

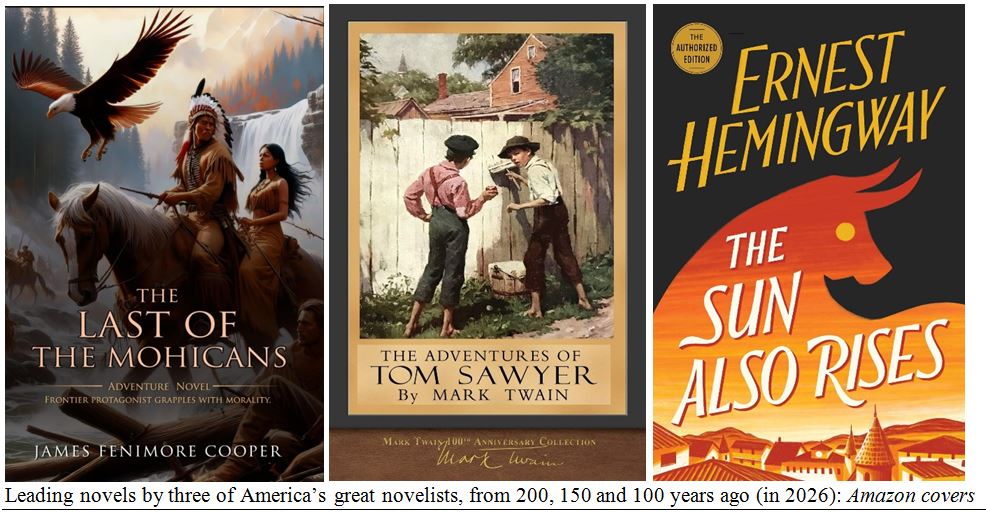

In closing this review, may I recommend three of our greatest novelists who published their first or greatest works precisely 200, 150 and 100-years ago, as measured from the coming year of 2026:

- On February 4, 1826, James Fenimore Cooper published “The Last of the Mohicans.”

- On June 9, 1876: Mark Twain published “The Adventures of Tom Sawyer.”

- On October 22, 1926, Ernest Hemingway debuted with “The Sun Also Rises.”

This handful of books and pamphlets from U.S. history ought to be part of a reading list for America 250.

All content above represents the opinion of Gary Alexander of Navellier & Associates, Inc.

Also In This Issue

A Look Ahead by Louis Navellier

What Could Go Wrong in 2026?

Income Mail by Bryan Perry

A Year-End Look Under the Market’s AI Hood

Growth Mail by Gary Alexander

U.S. GDP is Now Flirting With 5% Growth Rates in 2026

Global Mail by Ivan Martchev

Knocking on the Door of S&P 7000

Sector Spotlight by Jason Bodner

Santa Claus Arrives – Better Late Than Never

View Full Archive

Read Past Issues Here

About The Author

Gary Alexander

SENIOR EDITOR

Gary Alexander has been Senior Writer at Navellier since 2009. He edits Navellier’s weekly Marketmail and writes a weekly Growth Mail column, in which he uses market history to support the case for growth stocks. For the previous 20-years before joining Navellier, he was Senior Executive Editor at InvestorPlace Media (formerly Phillips Publishing), where he worked with several leading investment analysts, including Louis Navellier (since 1997), helping launch Louis Navellier’s Blue Chip Growth and Global Growth newsletters.

Prior to that, Gary edited Wealth Magazine and Gold Newsletter and wrote various investment research reports for Jefferson Financial in New Orleans in the 1980s. He began his financial newsletter career with KCI Communications in 1980, where he served as consulting editor for Personal Finance newsletter while serving as general manager of KCI’s Alexandria House book division. Before that, he covered the economics beat for news magazines. All content of “Growth Mail” represents the opinion of Gary Alexander

Important Disclosures:

Although information in these reports has been obtained from and is based upon sources that Navellier believes to be reliable, Navellier does not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Navellier’s judgment as of the date the report was created and are subject to change without notice. These reports are for informational purposes only and are not a solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in these reports must take into account existing public information on such securities or any registered prospectus.To the extent permitted by law, neither Navellier & Associates, Inc., nor any of its affiliates, agents, or service providers assumes any liability or responsibility nor owes any duty of care for any consequences of any person acting or refraining to act in reliance on the information contained in this communication or for any decision based on it.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any securities recommendations made by Navellier. in the future will be profitable or equal the performance of securities made in this report. Dividend payments are not guaranteed. The amount of a dividend payment, if any, can vary over time and issuers may reduce dividends paid on securities in the event of a recession or adverse event affecting a specific industry or issuer.

None of the stock information, data, and company information presented herein constitutes a recommendation by Navellier or a solicitation to buy or sell any securities. Any specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. The holdings identified do not represent all of the securities purchased, sold, or recommended for advisory clients and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Information presented is general information that does not take into account your individual circumstances, financial situation, or needs, nor does it present a personalized recommendation to you. Individual stocks presented may not be suitable for every investor. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Investment in fixed income securities has the potential for the investment return and principal value of an investment to fluctuate so that an investor’s holdings, when redeemed, may be worth less than their original cost.

One cannot invest directly in an index. Index is unmanaged and index performance does not reflect deduction of fees, expenses, or taxes. Presentation of Index data does not reflect a belief by Navellier that any stock index constitutes an investment alternative to any Navellier equity strategy or is necessarily comparable to such strategies. Among the most important differences between the Indices and Navellier strategies are that the Navellier equity strategies may (1) incur material management fees, (2) concentrate its investments in relatively few stocks, industries, or sectors, (3) have significantly greater trading activity and related costs, and (4) be significantly more or less volatile than the Indices.

ETF Risk: We may invest in exchange traded funds (“ETFs”) and some of our investment strategies are generally fully invested in ETFs. Like traditional mutual funds, ETFs charge asset-based fees, but they generally do not charge initial sales charges or redemption fees and investors typically pay only customary brokerage fees to buy and sell ETF shares. The fees and costs charged by ETFs held in client accounts will not be deducted from the compensation the client pays Navellier. ETF prices can fluctuate up or down, and a client account could lose money investing in an ETF if the prices of the securities owned by the ETF go down. ETFs are subject to additional risks:

- ETF shares may trade above or below their net asset value;

- An active trading market for an ETF’s shares may not develop or be maintained;

- The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track;

- The cost of owning shares of the ETF may exceed those a client would incur by directly investing in the underlying securities; and

- Trading of an ETF’s shares may be halted if the listing exchange’s officials deem it appropriate, the shares are delisted from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Grader Disclosures: Investment in equity strategies involves substantial risk and has the potential for partial or complete loss of funds invested. The sample portfolio and any accompanying charts are for informational purposes only and are not to be construed as a solicitation to buy or sell any financial instrument and should not be relied upon as the sole factor in an investment making decision. As a matter of normal and important disclosures to you, as a potential investor, please consider the following: The performance presented is not based on any actual securities trading, portfolio, or accounts, and the reported performance of the A, B, C, D, and F portfolios (collectively the “model portfolios”) should be considered mere “paper” or pro forma performance results based on Navellier’s research.

Investors evaluating any of Navellier & Associates, Inc.’s, (or its affiliates’) Investment Products must not use any information presented here, including the performance figures of the model portfolios, in their evaluation of any Navellier Investment Products. Navellier Investment Products include the firm’s mutual funds and managed accounts. The model portfolios, charts, and other information presented do not represent actual funded trades and are not actual funded portfolios. There are material differences between Navellier Investment Products’ portfolios and the model portfolios, research, and performance figures presented here. The model portfolios and the research results (1) may contain stocks or ETFs that are illiquid and difficult to trade; (2) may contain stock or ETF holdings materially different from actual funded Navellier Investment Product portfolios; (3) include the reinvestment of all dividends and other earnings, estimated trading costs, commissions, or management fees; and, (4) may not reflect prices obtained in an actual funded Navellier Investment Product portfolio. For these and other reasons, the reported performances of model portfolios do not reflect the performance results of Navellier’s actually funded and traded Investment Products. In most cases, Navellier’s Investment Products have materially lower performance results than the performances of the model portfolios presented.

This report contains statements that are, or may be considered to be, forward-looking statements. All statements that are not historical facts, including statements about our beliefs or expectations, are “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. These statements may be identified by such forward-looking terminology as “expect,” “estimate,” “plan,” “intend,” “believe,” “anticipate,” “may,” “will,” “should,” “could,” “continue,” “project,” or similar statements or variations of such terms. Our forward-looking statements are based on a series of expectations, assumptions, and projections, are not guarantees of future results or performance, and involve substantial risks and uncertainty as described in Form ADV Part 2A of our filing with the Securities and Exchange Commission (SEC), which is available at www.adviserinfo.sec.gov or by requesting a copy by emailing info@navellier.com. All of our forward-looking statements are as of the date of this report only. We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. You are urged to carefully consider all such factors.

FEDERAL TAX ADVICE DISCLAIMER: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Navellier to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Navellier does not advise on any income tax requirements or issues. Use of any information presented by Navellier is for general information only and does not represent tax advice either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

IMPORTANT NEWSLETTER DISCLOSURE:The hypothetical performance results for investment newsletters that are authored or edited by Louis Navellier, including Louis Navellier’s Growth Investor, Louis Navellier’s Breakthrough Stocks, Louis Navellier’s Accelerated Profits, and Louis Navellier’s Platinum Club, are not based on any actual securities trading, portfolio, or accounts, and the newsletters’ reported hypothetical performances should be considered mere “paper” or proforma hypothetical performance results and are not actual performance of real world trades. Navellier & Associates, Inc. does not have any relation to or affiliation with the owner of these newsletters. There are material differences between Navellier Investment Products’ portfolios and the InvestorPlace Media, LLC newsletter portfolios authored by Louis Navellier. The InvestorPlace Media, LLC newsletters contain hypothetical performance that do not include transaction costs, advisory fees, or other fees a client might incur if actual investments and trades were being made by an investor. As a result, newsletter performance should not be used to evaluate Navellier Investment services which are separate and different from the newsletters. The owner of the newsletters is InvestorPlace Media, LLC and any questions concerning the newsletters, including any newsletter advertising or hypothetical Newsletter performance claims, (which are calculated solely by Investor Place Media and not Navellier) should be referred to InvestorPlace Media, LLC at (800) 718-8289.

Please note that Navellier & Associates and the Navellier Private Client Group are managed completely independent of the newsletters owned and published by InvestorPlace Media, LLC and written and edited by Louis Navellier, and investment performance of the newsletters should in no way be considered indicative of potential future investment performance for any Navellier & Associates separately managed account portfolio. Potential investors should consult with their financial advisor before investing in any Navellier Investment Product.

Navellier claims compliance with Global Investment Performance Standards (GIPS). To receive a complete list and descriptions of Navellier’s composites and/or a presentation that adheres to the GIPS standards, please contact Navellier or click here. It should not be assumed that any securities recommendations made by Navellier & Associates, Inc. in the future will be profitable or equal the performance of securities made in this report.

FactSet Disclosure: Navellier does not independently calculate the statistical information included in the attached report. The calculation and the information are provided by FactSet, a company not related to Navellier. Although information contained in the report has been obtained from FactSet and is based on sources Navellier believes to be reliable, Navellier does not guarantee its accuracy, and it may be incomplete or condensed. The report and the related FactSet sourced information are provided on an “as is” basis. The user assumes the entire risk of any use made of this information. Investors should consider the report as only a single factor in making their investment decision. The report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. FactSet sourced information is the exclusive property of FactSet. Without prior written permission of FactSet, this information may not be reproduced, disseminated or used to create any financial products. All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index. Past performance is no guarantee of future results.